http://www.kingworldnews.com/kingworldnews/Broadcast_Gold+/Entries/2010/7/26_Jim_Rickards.html

http://kingworldnews.com/kingworldnews/Broadcast_Gold+/Entries/2010/7/28_Jim_Rickards__Part_II.html

This one too sent in by Shaza

'Black Swan' author Taleb sees government debt as 'pure Ponzi scheme'

A “black swan” event, as made indelible in popular culture by scholar and former Wall Street traderNassim Taleb, is an extraordinarily rare occurrence of massive magnitude and consequence.

That made Taleb’s 2007 book, “The Black Swan: The Impact of the Highly Improbable,” the perfect set-up for the financial-system crash of 2008.

Except that Taleb has said repeatedly that the crash was not a black swan, because extreme risk-taking in the banking system had made a crisis “unavoidable . . . just as a drunk and incompetent pilot would eventually crash the plane.” See this rant on his blog.

Now, in an interview with Bloomberg Businessweek, Taleb sees the same pattern in soaring government debt levels.

But Taleb implies the same inevitability of disaster. From theBloomberg interview:

Well, not quite in the case of the U.S. Treasury: For the moment there is no shortage of demand for Uncle Sam’s debt, which is why long-term Treasury yields are near 15-month lows.Q. What are are potential sources of fragility or danger that you're keeping an eye on?A. The massive one is government deficits. As an analogy: You often have planes landing two hours late. In some cases, when you have volcanos, you can land two or three weeks late. How often have you landed two hours early? Never. It's the same with deficits. The errors tend to go one way rather than the other.The problem is getting runaway. It's becoming a pure Ponzi scheme. It's very nonlinear: You need more and more debt just to stay where you are. And what broke [convicted financier Bernard] Madoff is going to break governments. They need to find new suckers all the time. And unfortunately the world has run out of suckers.

In any case, Taleb doesn't offer any novel advice to investors who fear a government-debt crisis. He recommends keeping cash in short-term Treasury bills.

“Because governments can print more of their own currency, the risk comes from a rise in interest rates rather than a government default,” he notes. “When you have hyperinflation, deficits, or debt problems, with short-term bills you can catch higher interest rates to compensate you for the inflation or whatever return you've missed.”

Taleb, who says on his blog that he now is “bored with finance,” tells Bloomberg his next book will be “about beliefs, mostly. How we are suckers and how to live in a world we don't understand.”

Along those lines, he says most people have no business investing in the stock market except with money they're willing to lose.

"The problem is that citizens are being led to invest in securities they don't understand by people who themselves don't quite understand the risks involved," he says. "The stock market is probably the best thing in the world, but the true risks of the stock market are vastly greater than the representations."

-- Tom Petruno

Companies hold record $837B in cash, yet won't hire workers Thanks Shaza

By Matt Krantz, USA TODAY

Anyone wondering where all the economy's jobs are might want to look into piggy banks of the world's biggest companies.

Cash is gushing into companies' coffers as they report what's shaping up to be the third-consecutive quarter of sharp earnings increases. But instead of spending on the typical things, such as expanding and hiring people, companies are mostly pocketing the money and stuffing it under their corporate mattresses.

Non-financial companies in the Standard & Poor's 500 have a record $837 billion in cash, S&P says. That's enough to pay 2.4 million people $70,000-a-year salaries for five years. For context, 2.2 million to 2.8 million jobs were saved or created by the $862 billion stimulus that President Obama signed into law in February 2009, according to a report released in April from the Council of Economic Advisers.

Rather than investing in their future, companies are piling up cash and collecting practically zero interest on the money, hoping there will be a better time to invest later.

WHERE ARE THE JOBS? Latest forecast for 384 metro areas and all 50 states

The stockpiling of cash is troubling to some, who say that if companies keep hoarding money instead of investing in new facilities and products, it will put a lid on what the economy really needs to get going: new jobs. "Managers are being overly conservative until they're positive the crisis is over," says Kathleen Kahle, professor of finance at the University of Arizona. "They don't want to invest and add jobs, so they're delaying and don't want to be the first movers."

Meanwhile, there's concern companies have starved expansion so long, and focused merely on cutting costs to boost short-term profit, many might have difficultly boosting their top lines. "Reducing costs is a one-trick pony," says George Christy, principal of financial advisory firm Oakdale Advisors and author of Free Cash Flow. "You can only hold down headcount so much without hurting the quality of your products."

A shocking buildup of funds

The level of cash being built up by companies is staggering. Companies' cash piles are:

•Bigger than ever. The $837 billion in cash and short-term investments non-financial S&P 500 companies hold as of the first quarter, the latest data available, is not only a record, but up 26% from $665 billion a year ago, says Howard Silverblatt of S&P.

•Massive compared with companies' market values.Companies are holding cash equal to 10% of their total value, Silverblatt says. That's up from normal levels: Since 1999 companies held cash equal to 6.6% of their value on average.

•Dwarfing money spent on investments. Non-financial S&P 500 companies invested $130 billion on new facilities and equipment in the fourth quarter of 2009, the latest data available from S&P. That's an improvement from the previous three quarters, but down 12% from the levels a year earlier.

And it's not as though companies are rapidly boosting dividends or buying back their stock. S&P 500 companies paid $50.4 billion in dividends in the second quarter, up 5.9% from a year ago but up just 2.3% from the first quarter and well below the $67 billion paid in late 2007, S&P says.

Merger and acquisition activity, another major use of corporate cash, is also slow to recover. Companies spent more than $411 billion buying U.S. companies this year through the second quarter, down 9.5% from the same year-ago period, Dealogic says.

Scared to spend

Companies continue to stockpile cash, in part, because they don't want to be caught in a bind like many were when credit markets froze in late 2007 through 2009, says Lee Pinkowitz, finance professor at Georgetown University. "Companies want cash for a rainy day," he says. "People didn't realize how rainy it could get."

Meanwhile, cash is ballooning as technology companies have a more significant presence in the economy, Kahle says. Most of the biggest holders of cash are technology firms, including Cisco Systems (CSCO),Microsoft (MSFT), Google (GOOG), Apple (AAPL), Oracle (ORCL) and Intel (INTC), which routinely hold big cash piles to prepare for a sudden shift in technology.

Meanwhile, investors are being more patient than usual with cash-rich companies.

Investors don't want companies to rush out and invest and hire just because they have cash, says Marc Gerstein, research consultant for market data provider Portfolio 123. "Getting a low return on cash is the second-worst thing companies can do. The worst thing is to waste the cash."

Waiting for right opportunity

Some companies say they're ready to use their cash as soon as there are opportunities. Intel, the massive computer chipmaker, ended its most recent quarter with more than $18 billion in cash and investments that can quickly be turned into cash, up from $11.6 billion a year ago, which puts it in the top 10 of cash-rich S&P 500 companies. "Intel is a cash-generating machine," says Patrick Wang of Wedbush Securities.

Intel is holding cash so it's ready to build manufacturing plants, which cost upward of $4 billion, when needed, spokesman Tom Beermann says. The company also pays a 3% dividend yield, which is higher than the average paid by other technology firms. Intel also stands ready to make investments.

And online retailer Priceline (PCLN), which ended its most recent quarter with $1.2 billion in cash, paid down $500 million in debt the past several years, spent hundreds of millions of acquisitions, including recently TravelJigsaw, and bought back $100 million in stock in the first quarter.

Once companies get more comfortable about the economy's future, the hoarding mentality might ease a bit, Kahle says. "Cash can't increase indefinitely. If cash is 100% of assets, then firms aren't doing anything.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Americans Splurge on IPads While Broke in New Abnormal Economy

I don't know whether to laugh or cry when I read stories like these. Queenbee

By Devin Leonard

By Devin Leonard

July 30 (Bloomberg) -- In March, Ralph Ronzio went to a warehouse in a seedy part of Orange County, California, and watched a man auction off his condo for half what he’d paid for it. Ronzio had bought the place for $329,000 in 2005, when he moved to Southern California from Rhode Island to take a job at a data-storage company. It was the first place he’d ever owned.

“It was totally my bachelor pad,” he says. “Not much inside other than the usual leather couch and the big screen TV. My fiancée made me sell the couch.”

That wasn’t the only thing that changed when Ronzio got engaged. His fiancée had two young children, and there wasn’t enough room in the condo for all four of them. So last year, Ronzio bought a house nine miles (14 kilometers) away and they all moved in. He figured he could rent the condo and cover his costs. He figured wrong, Bloomberg Businessweek reports in its Aug. 2 issue.

The more he thought about the money he was losing, the more it stressed him out. Finally, Ronzio enlisted the help of a firm called You Walk Away and did exactly that from the remaining $319,000 on his condo mortgage. When the bank foreclosed, he says he felt a sense of relief. He also had more cash. He and his fiancée took the kids to Disneyland. Ronzio, 31, gave himself a treat as well.

“I bought myself an iPad,” he says.

Latest Apple Gadget

It used to be that someone like Ronzio could be fairly certain of the outcome when spending a few hundred thousand dollars on real estate. Housing prices were headed in only one direction. You could surf the boom and borrow against your home equity to pay for all manner of splurges -- a vacation, a flat- screen television, or the latest Apple Inc. gadget. Considering that housing prices almost doubled from 1999 to 2006, there was always an escape hatch: Sell your house and make enough money to pay it all back.

That was the old normal. Last year, Mohamed El-Erian, chief executive officer of Pacific Investment Management Co., manager of the world’s biggest bond fund, declared a “new normal,” a global realignment in which the U.S. consumer, no longer a hungry monster, became cautious and subdued.

The current circumstances might be better described as the new abnormal, in which no one knows anything. In June, the Conference Board Consumer Confidence Index fell 9 points after an 11 percent drop in the S&P 500 the month before. New housing starts were at an eight-month low. Meanwhile, the unemployment rate still hovers near double digits. That’s 14.6 million Americans out of work. Federal Reserve Chairman Ben Bernanke added to the anxiety with a July 21 declaration that the economic outlook is “unusually uncertain.”

‘Liquidity-Constrained’

So who are all those people at the mall? It’s easy to forget that a 9.5 percentunemployment rate means that about 9 out of 10 Americans in the workforce are still employed.

“Some consumers are probably liquidity-constrained,” says Kenneth Rogoff, Harvard University professor and former chief economist at the International Monetary Fund. These are “the ones who are probably not the ones buying iPads. But 90 percent of Americans do have a job, and maybe 70 percent are confident about them. And maybe half of those have liquidity.”

On a recent afternoon, Lucy Johnston, 37, an accountant from Tulsa, Oklahoma, could be found at the Fashion Show mall on the Strip in Las Vegas. She’s cutting back on shopping and eating out because of the recession.

“It’s really tough right now,” Johnston says. “I don’t do many full-on spa days anymore.”

Yet there she was, shopping and vacationing in Vegas with her husband.

“We’ve pulled out all the stops. We’re staying at the Bellagio,” she says.

Schizophrenic Consumers

The new abnormal has given rise to a nation of schizophrenic consumers. They splurge on high-end discretionary items and cut back on brand-name toothpaste and shampoo. Companies such as Cupertino, California-basedApple, whose net income jumped 94 percent in its last quarter, and Starbucks Corp., which saw a 61 percent increase in operating income over the same time frame, are thriving.

Mercedes-Benz is having a record sales year; deliveries of new vehicles in the U.S. rose 25 percent in the first six months of 2010. Lexus and BMW were also up. Though luxury-goods manufacturers such as Hermes International SCAand Burberry Group Plc are looking primarily to Asia for growth, their recent earnings reports suggest stabilization and even modest improvement in the U.S.

Bifurcated Market

“Last September, retail started to recover on a very narrow basis,” saysMichael Niemira, chief economist for the International Council of Shopping Centers. “Most of the industry was really weak. It wasn’t until the end of the year that you saw any momentum. It was all dollar stores and luxury. You have this bifurcated market. This year, it started to move to the middle a little. Now it’s kind of moved back to the edges.”

Some of this is a reminder that the rich have been largely shielded from the recession’s ravages.

“All of my customers think we are out of the recession,” says Marika Baca, an associate in the women’s department at the Barneys New York store. “This time last year, it was bad. But now the women who were reluctantly picking up one piece are easily buying three.”

Aspirational middle-class consumers say they are also yearning to get their hands on the same high-end merchandise, just as they did in better times.

Family Dollar Stores

In such an environment, optimism about the economic future ebbs and flows constantly, with far-reaching consequences for a nation in which consumer spending accounts for 70 percent of the gross national product. It’s an economy that suggests an EKG- shaped recovery -- a sequence of mini booms and busts as consumer fads and pent-up demand drive sales, until the impulses fade. Erratic behavior is everywhere, even at Matthews, North Carolina-based Family Dollar Stores Inc.

“My feeling is that you can see week-to-week differences today that are far more volatile than what we have been seeing,” says R. James Kelly, the company’s president and chief operating officer, reporting a quarter with a 19 percent increase in net income.

Consumer confidence was edging up earlier this year. The stock market had rebounded. It looked like the economy took on aspects of normal behavior -- and then it all fell apart. In June, the stock market gave back 4 percent of its value. Like teenagers suffering mood swings, consumers lost their nerve all over again.

‘Dark Cloud’

On July 27, the Conference Board reported that confidence was at a five-month low, which it blamed on job insecurity.

“Concerns about the labor market are casting a dark cloud over consumers that is not likely to lift until the job market improves,” Lynn Franco, director of the board’s consumer research center, says in a statement.

Not everybody’s consumer diagnosis is the same, though. Shortly before the Conference Board released its finding, Consumer Reports, the 74-year-old magazine, unveiled the results of its monthly telephone survey about economic issues. It found that consumers had ramped up their retail spending by an average of $40. Though major purchases like cars remained unlikely, Americans were planning to spend more on appliances and electronics.

“We just focus on what’s happening this month,” says Ed Farrell, a director of the Consumer Reports National Research Center. “We don’t ask people what they think the business climate is going to be like in a year. If these people could tell us that, we’d all be very well off.”

Consumer Survey

American Express Co. released the results of its consumer survey on July 13, showing more willingness to spend, damped somewhat by guilt and despair on the part of some of these same respondents. The New York-based credit-card company found that 51 percent of consumers had fallen behind on their annual savings plan, in part because they were either making impulse purchases or simply spending beyond their means. There it is: gloom, muted optimism, and wild abandon.

What if these things aren’t exclusive in the new abnormal? Frank Veneroso, an investment strategy adviser in Portsmouth, New Hampshire, follows the nation’s saving rate. It was his opinion that high debt levels and economic fears would force Americans to rein in their spending and increase their savings.

‘Celebratory Spending Spree’

In the early part of the recession, that’s what happened. Then it stopped happening. Veneroso writes in a report that the nation’s wealthier citizens were so relieved when the stock market rallied last year after the financial crisis that they went on a “celebratory spending spree.” The recent market turmoil will put a stop to it and savings will start to inch back up, Veneroso says.

Except market rallies aren’t the only thing that emboldens consumers. Market dips can also loosen up purse strings, says Dan Ariely, a professor of behavioral economics at Duke University and author of “Predictably Irrational: The Hidden Forces that Shape Our Decisions.” When people fret about market gyrations, they see the advantage of shopping over putting money into a mutual fund that might tank, Ariely says.

“If they lose money by spending it on something, at least they have something to show for it,” he says.

For consumers looking for a reason, ups and downs can both provide a justification for spending. Stephanie Redmond, a 25- year-old electronics worker, talked about her financial woes as she shopped at the Dolphin Mall in Miami. She described herself as pessimistic about the economy.

Need New Car

“I don’t see it getting any better,” she said. “I need a new car, but I don’t plan on getting one anytime soon.”

Instead she recently bought a plane ticket to New York and stayed in a Times Square hotel.

“It was my first time, so it was a lot of fun,” she said.

At the Woodfield Shopping Center in Schaumburg, Illinois, Michelle Rodriguez, 39, a part-time cafeteria worker at a local high school, said she cut back considerably after losing her old full-time job two years ago as a receptionist at Kraft Foods Inc.

“I think the economy has a ways to go,” she said. “I don’t make nearly as much as I used to make.”

Yet she said she bought a 46-inch flat-screen Sony TV in the last year. And now she was waiting for help in the Genius Bar line at the Apple Store.

Apple Revenue

One way of understanding Apple’s recent success -- the company announced “all-time record” revenue of $15.7 billion for its quarter ending on June 26 -- is that the iPad is positioned as a compromise product for people who crave the kick of a new Apple gadget and don’t want to spring for a Mac.

“I was talking to someone recently who said to me, ‘I bought the iPad because I can’t afford a new iMac,’” says Carla Serrano, chief strategist for TBWA/Chiat/Day, Apple’s advertising agency. “O.K., fine. But the iPad does hardly anything that an iMac can do.”

The recession is making people think they need to come up with that she describes as “post-rational” justifications for their extravagant purchases, she says.

The performance of Seattle-based Starbucks suggests that everyday luxuries have also not been wiped out. On July 21, the coffee chain announced a “record” quarter with same-store sales growth of 9 percent, the biggest increase since the second quarter of 2006, the peak of the old normal.

CEO Howard Schultz highlighted Starbucks’ new products, like the “customizable Frappuccino campaign,” as well as Via, the new instant coffee, which is pitched as a budget item, though not exactly priced like one when compared with other instant competitors. A 12-packet box of Via goes for $9.95.

‘Every day!’

Starbucks is the lower-end corollary to Apple, a purveyor of expensive treats. Stephanie Redmond, the Miami electronics worker, may not buy the new car she needs, but give up Starbucks? Never. She says she has to have it “every day!”

Mass marketers have a tougher time seducing consumers with psychological value. Burt Flickinger, a retail consultant based in New York, says Procter & Gamble Co. is struggling to keep people from abandoning its Ivory soap and Crest toothpaste for generic brands. According to Flickinger, better-educated shoppers understand how little difference there is in quality on many household items.

They may also be sneaking into discount retailers for these deals.

Cheap Towels

“The dollar store is the new Target,” says Al Moffatt, CEO of Worldwide Partners, a Denver-based advertising company. “You go in there to buy shampoo for a buck so you can go to Starbucks and justify spending $3 for a coffee.”

Moffatt says that he and his wife recently did their own variation on this recessionary theme. On a trip to Oregon, they bought cheap towels at a discount store before hitting a pricey spa.

Ran Kivetz, a professor of marketing at Columbia Business School, has done research on consumer psychology. He says that consumers’ brains lack a line that separates spending from saving. We practice a certain amount of thrift so that we can justify blowing a large sum frivolously, he says.

Kivetz says the recent recession has made consumer thinking even more conflicted. In the short run, we feel good when we save. In the long run, we tend to regret the denial of a spending outlet.

“We feel guilty” about spending, Kivetz says, which can lead to more irrational purchasing.

Need to Spend

That’s is exactly what’s happening now, according to Kivetz. Consumers were quick to reduce spending when the recession arrived. Then the recession lasted longer than expected, and the new abnormal set in. The economy started to improve. Then it appeared to worsen. There is only so long we can suppress our need to spend, Kivetz says.

“It’s just been a slow walk out of the woods,” he says. “And it’s so complicated. The things going on in Europe are frightening. There are problems with China, with our government debt, and bank debt. At the end of the day, people are saying, ‘There is still risk. I gotta cut back.’ But this is not a typical one-year recession. Life has to have some normalcy. I have to have some luxuries.”

There was little evidence of the recession at a recent lunchtime in the Mall of America in Bloomington, Minnesota. The nation’s largest mall was full of shoppers drinking expensive coffee and toting bags of electronics and expensive shoes. Some of them were there on vacation. Why not? The Mall of America doesn’t just have 520-plus shops, it has an enormous amusement park and a 1.2 million gallon aquarium. Sales are up 9 percent so far this year.

Mellissa Williams, a 30-year-old teacher from Laredo, Missouri, was looking for sneakers with her two children at a sporting goods store.

“We’ll be looking at price tags a little more than we normally would,” she said.

And yet she had come a long way to look for deals. What was her biggest splurge in the last six months?

“Probably this trip,” Williams said.

Morning Update/ Market Thread 7/30

Good Morning,

Equity futures are down this morning following the release of second quarter GDP. The dollar is up slightly, bonds are higher, oil is down, and gold is higher.

The GDP number came in at 2.4% while the consensus called for 2.5%. Q1 was revised upward a full percentage point, however, to 3.7%! Not only that, but the past 3 years growth numbers were revised! Hey, if you can’t stand the truth, just make something up – it is now a time honored tradition in money, politics, and economic statistics.

As if the GDP numbers weren’t already grossly overstated enough via manipulations with inflation and the “deflator,” and by including financial engineering as productivity. The bottom line is that even with their manipulations, the trend is down and I think by the 3rd quarter it is likely to turn negative again – the ECRI has not been wrong yet with readings such as are occurring now. Here’s Econoday attempting to convince you otherwise:

The price index rising much stronger than expected I think reflects the recent bounce higher in oil prices. Still, that reading needs to be watched as it can pressure interest rates. Overall this report is about what I expected, a manipulated and heavily massaged attempt to placate the public.

Chicago PMI and Consumer Sentiment come out just prior to 10 Eastern.

And the world just gets even more bizarre by the day. Yesterday an idea surfaced from a MS analyst that the GSEs should simply reset every prime mortgage held to the lowest possible market rate! This would lower monthly payments and stimulate the economy according to his theory. And actually it would put more money into the hands of a few consumers, it would help the banks on one hand, but it may hurt the holders of bond and derivative holders. It would be yet another moral hazard that ultimately keeps real estate overpriced for longer, and thus it’s an idea that I certainly hope does not come to pass.

Moody’s says that Spain will likely lose their triple-A rating and that it’s time for the U.S. to develop a clear plan regarding our deficits. This warning is pressuring equities.

Additionally, the IMF says that it completed its mini stress test on U.S. banks and that our banks will likely need to raise additional capital. Here’s a snippet from Bloomberg:

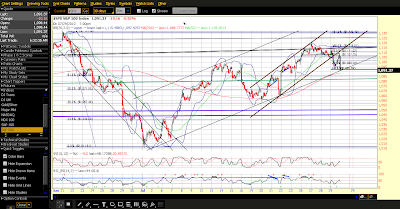

The up, down, up action yesterday broke what I was tracking as the wave c channel, but did not break beneath the larger wave 2 channel. The 30 minute chart below shows these, note that the opening print fell exactly on the bottom of the larger channel, so be careful:

McHugh still believes yesterday was a part of a wave 4 movement, and that should prices fall beneath 10,300 on the DOW that it’s his clue that wave 3 has begun. I personally don’t see how we could still be in wave 4 as the smaller channel break means that we have likely turned into the next wave. For me, a break below the larger channel means that wave 2 is likely done and that we have entered wave 3. Regardless, it appears that the 1115 area and the 50% retrace stopped the advance without making new intraday highs and now we are likely turning.

The VIX is attempting to break above its descending upper trendline, a clean break above that line is very bearish for the market:

Bonds are substantially higher showing that money is once again flowing to “safety.” Keep in mind that today is Friday and that the HFT machines are programmed to Pavlov the market prior to the close in anticipation of the coming Monday ramp job. At some point the dog is going to run out of treats, I hope that comes sooner than later as that trend is definitely tiresome.

Equity futures are down this morning following the release of second quarter GDP. The dollar is up slightly, bonds are higher, oil is down, and gold is higher.

The GDP number came in at 2.4% while the consensus called for 2.5%. Q1 was revised upward a full percentage point, however, to 3.7%! Not only that, but the past 3 years growth numbers were revised! Hey, if you can’t stand the truth, just make something up – it is now a time honored tradition in money, politics, and economic statistics.

As if the GDP numbers weren’t already grossly overstated enough via manipulations with inflation and the “deflator,” and by including financial engineering as productivity. The bottom line is that even with their manipulations, the trend is down and I think by the 3rd quarter it is likely to turn negative again – the ECRI has not been wrong yet with readings such as are occurring now. Here’s Econoday attempting to convince you otherwise:

HighlightsA part of the revised data shows that the “recession” of 2007 to 2009 was worse than previously reported, with growth revised downward for that period – part of the trend is to under report weakness, then revise it lower later.

Despite all of the doomsayers, the recovery continued in the second quarter but at a moderate pace. Yes, the recovery is still below par but it's not a double dip so far. Second quarter GDP came in at an annualized 2.4 percent growth, following a revised first quarter gain of 3.7 percent. Today's release includes annual revisions going back three years. The second quarter advance estimate is just barely below analysts' projections for a 2.5 percent increase. But the first quarter upward revision of a full percentage point from the prior estimate of 2.7 percent is a positive surprise.

The latest quarter was led by a rebound in residential investment, a jump in investment in equipment & software, and by inventories. PCEs also posted a moderate gain along with government purchases. The big negative is a worsening in net exports.

Real final sales to domestic purchasers rose 1.3 percent, compared to up 1.1 percent in the first quarter.

Final sales of domestic product gained an annualized 4.1 percent in the second quarter, following a 1.3 percent rise the prior quarter. Final sales to domestic purchasers exclude inventory investment but include sales to consumers in the U.S., business fixed investment, residential investment, and government purchases. Final sales of domestic product include final sales to domestic purchasers and add in net exports (GDP less inventory investment).

Economy-wide inflation accelerated in the second quarter as the GDP price index rose an annualized 1.8 percent, following a 1.0 percent in the first quarter. The market forecast called for a 1.0 percent gain.

Overall, the recovery is stronger than believed but markets reacted adversely to the headline number for the latest quarter being soft.

The price index rising much stronger than expected I think reflects the recent bounce higher in oil prices. Still, that reading needs to be watched as it can pressure interest rates. Overall this report is about what I expected, a manipulated and heavily massaged attempt to placate the public.

Chicago PMI and Consumer Sentiment come out just prior to 10 Eastern.

And the world just gets even more bizarre by the day. Yesterday an idea surfaced from a MS analyst that the GSEs should simply reset every prime mortgage held to the lowest possible market rate! This would lower monthly payments and stimulate the economy according to his theory. And actually it would put more money into the hands of a few consumers, it would help the banks on one hand, but it may hurt the holders of bond and derivative holders. It would be yet another moral hazard that ultimately keeps real estate overpriced for longer, and thus it’s an idea that I certainly hope does not come to pass.

Moody’s says that Spain will likely lose their triple-A rating and that it’s time for the U.S. to develop a clear plan regarding our deficits. This warning is pressuring equities.

Additionally, the IMF says that it completed its mini stress test on U.S. banks and that our banks will likely need to raise additional capital. Here’s a snippet from Bloomberg:

July 30 (Bloomberg) -- The U.S. financial system remains fragile and banks subjected to additional economic stress might need as much as $76 billion in capital, according to the results of International Monetary Fund stress tests.Since the IMF is comprised of the same central banks that they are “stress testing,” isn’t this the kettle calling itself black? So what’s their game this time? Let’s revisit that last paragraph… they want the government to “take over the GSEs’ public housing mission while privatizing investment operations.” Uh, huh. In other words, they want the taxpayer to pick up the tab while they run their high leverage games all backstopped by you and me… that’s their game, and they absolutely need to be stopped. Again, with no adult supervision to be found, the criminals continue to run their Ponzi schemes.

The findings, released today as part of a broader IMF report on the U.S. financial system, suggested that while the nation’s banking system is stable, it remains vulnerable. Home prices, commercial real estate loans and economic growth have the potential to cause shocks that could expose banks to more losses.

Under one scenario, small and regional banks as well as subsidiaries of foreign banks would need $40.5 billion in additional capital to meet a benchmark capital ratio of 6 percent Tier 1 common equity from 2010 to 2014. Under the adverse scenario, those needs rise to $76.3 billion, according to the report.

“Pockets of vulnerabilities linger,” the fund said in the report. The U.S. is recovering from what the IMF called “one of the most devastating financial crises in a century.”

Because the economic recovery is proceeding slowly, regulators must be especially vigilant in guarding against risks and weak spots, the report said.

The IMF also renewed its call for the Obama administration to push ahead with changes to Fannie Mae and Freddie Mac, the government-sponsored enterprise housing companies. The report suggested a partial privatization strategy, in which the government would take over the GSEs’ public housing mission while privatizing investment operations.

The up, down, up action yesterday broke what I was tracking as the wave c channel, but did not break beneath the larger wave 2 channel. The 30 minute chart below shows these, note that the opening print fell exactly on the bottom of the larger channel, so be careful:

McHugh still believes yesterday was a part of a wave 4 movement, and that should prices fall beneath 10,300 on the DOW that it’s his clue that wave 3 has begun. I personally don’t see how we could still be in wave 4 as the smaller channel break means that we have likely turned into the next wave. For me, a break below the larger channel means that wave 2 is likely done and that we have entered wave 3. Regardless, it appears that the 1115 area and the 50% retrace stopped the advance without making new intraday highs and now we are likely turning.

The VIX is attempting to break above its descending upper trendline, a clean break above that line is very bearish for the market:

Bonds are substantially higher showing that money is once again flowing to “safety.” Keep in mind that today is Friday and that the HFT machines are programmed to Pavlov the market prior to the close in anticipation of the coming Monday ramp job. At some point the dog is going to run out of treats, I hope that comes sooner than later as that trend is definitely tiresome.

Decline and fall of the US Hat Tip to Nicolas Darvas

Niall Ferguson says the US is in the decline and in danger of falling. Photo: Dewald Aukema

In the history of empires the end is abrupt, and those that rely on them need to be ready.

All empires, no matter how magnificent, are condemned to decline and fall. We tend to assume that in our own time, too, history will move cyclically - and slowly.

The environmental or demographic threats we all talk about seem remote. In an election year, who really cares about the average atmospheric temperature or the age structure of the population in 2050?

Yet it is possible that this whole cyclical framework is, in fact, flawed. What if history is arrhythmic - at times almost stationary, but also capable of accelerating suddenly, like a sports car? What if collapse comes suddenly, like a thief in the night?

Great powers and empires operate somewhere between order and disorder. They can appear to operate quite stably for some time; they seem to be in equilibrium but are, in fact, constantly adapting. But a small trigger can set off a ''phase transition'' from a benign equilibrium to a crisis - a butterfly flaps its wings in the Amazon and brings about a hurricane in south-eastern England.

Regardless of whether it is a dictatorship or a democracy, any large-scale political unit is a complex system. Most great empires have a nominal central authority - either a hereditary emperor or an elected president - but in practice the power of any individual ruler is a function of the network of economic, social and political relations over which he or she presides.

As such, empires exhibit many of the characteristics of other complex adaptive systems - including the tendency to move from stability to instability quite suddenly. But this fact is rarely recognised because of our addiction to cyclical theories of history.

The Bourbon monarchy in France passed from triumph to terror with astonishing rapidity. French intervention on the side of the colonial rebels against British rule in North America in the 1770s seemed like a chance for revenge after Great Britain's victory in the Seven Years War a decade earlier, but it served to tip France into a critical state.

In May 1789, the summoning of the Estates-General, France's long-dormant representative assembly, unleashed a political chain reaction that led to a swift collapse of royal legitimacy in France. Only four years later, in January 1793, Louis XVI was decapitated by guillotine.

The sun set on the British Empire almost as suddenly. So, what are the implications for the United States today?

The most obvious point is that imperial falls are associated with fiscal crises - sharp imbalances between revenues and expenditures, and the mounting cost of servicing a mountain of public debt.

Think of Ottoman Turkey in the 19th century: debt service rose from 17 per cent of revenue in 1868 to 32 per cent in 1871 to 50 per cent in 1877, two years after the great default that ushered in the disintegration of the Ottoman Empire in the Balkans. Consider Britain in the 20th century. By the mid 1920s, debt charges were absorbing 44.5 per cent of total government expenditure, exceeding defence expenditure every year until 1937, when rearmament finally got under way in earnest.

But Britain's real problems came after 1945, when a substantial proportion of its immense debt burden - equivalent to about a third of gross domestic product - was in foreign hands.

Alarm bells should therefore be ringing loudly in Washington, as the US contemplates a deficit for 2010 of more than $US1.47 trillion - about 10 per cent of gross domestic product, for the second year running.

Since 2001, in the space of just 10 years, the US federal debt in public hands has doubled as a share of GDP from 32 per cent to a projected 66 per cent next year. It is projected that debt could reach 344 per cent by 2050.

These sums may sound fantastic. But more terrifying is to consider what continuing deficit finance could mean for the burden of interest payments as a share of federal revenues - up to 85 per cent in 2050.

The fiscal position of the US is worse than that of Greece. But Greece is not a global power. In historical perspective, unless something radical is done soon, the US is heading into into Bourbon France territory. It is heading into Ottoman Turkey territory. It is heading into postwar Britain territory.

For now, the world still expects the US to muddle through, eventually confronting its problems when, as Winston Churchill famously said, all the alternatives have been exhausted. With the sovereign debt crisis in Europe combining with growing fears of a deflationary double-dip recession, bond yields are at historic lows. There is therefore a strong incentive for those in the US Congress to put off fiscal reform.

Remember, half the US federal debt in public hands is in the hands of foreign creditors. Of that, a fifth (22 per cent) is held by the monetary authorities of the People's Republic of China, down from 27 per cent in July last year. China now has the second-largest economy in the world and is almost certain to be America's principal strategic rival this century, particularly in the Asia-Pacific region.

Quietly, discreetly, the Chinese are reducing their exposure to US Treasury bonds. Perhaps they have noticed what the rest of the world's investors pretend not to see - that the US is on an unsustainable fiscal course, with no apparent political means of self-correcting.

That has profound implications not only for the US, but also for all countries that have come to rely on it, directly or indirectly, for their security.

Niall Ferguson is a British historian and the author of The Ascent of Money. This is an edited version of his John Bonython Lecture for the Centre for Independent Studies delivered in Sydney last night.

Subscribe to:

Comments (Atom)