Morning Update/ Market Thread 10/29

Good Morning,

Equity futures are lower again this morning, the dollar is roughly flat, bonds are rising sharply, while oil is down slightly and gold is up.

Of course it’s pretty common knowledge that up trends typically end on good news, while downtrend end on bad news. These news events typically draw in the last rush for a given direction and produce capitulation volume. Such an event has still not happened and I think it’s very interesting how in the past couple of weeks or so the economic data has been read that if it’s bad it’s good because QE will save the world, and if it’s good it’s good. Then there are the numbers that come out EXACTLY on consensus, something that almost never happens yet there have been a string of these in the past week, this morning’s release of Q3 GDP is the latest.

Coming in exactly on consensus of 2.0% growth, look for quarter three GDP to be subsequently cut in half or more in future revisions. Q2 settled on 1.7%, and I can almost guarantee that Q3 was considerably slower than Q2. Keep in mind that GDP is measured in dollars and then “corrected” via the deflator for inflation. Again I’ll guarantee that the deflator comes nowhere near capturing the destruction that’s occurring to the dollar. Below is the entire report from the BEA:

Q3 GDP

What you will find inside that report is that inventory build resulted in the majority of the “growth,” 1.44%. Inventory builds are only good if there’s demand to buy the inventory once it’s produced. Forced inventory builds occur when goods are ordered due to miscalculations of demand. Demand is misjudged when economic data is artificial – thus bad tracking and reporting of data builds economic distortions, inventory building at this time is one.

You’ll also note in this report that almost every category tracked, while reported positive, is DECELERATING substantially from the prior report. Take exports for an example: “Real exports of goods and services increased 5.0 percent in the third quarter, compared with an increase of 9.1 percent in the second. Real imports of goods and services increased 17.4 percent, compared with an increase of 33.5 percent.” The numbers seem large, but are much smaller than the previous quarter. Again, they claim these numbers are “real,” that is adjusted for inflation, but again I have to raise the B.S. flag to full mast on those numbers. Shipping data and tax receipts do not substantiate their trade data that again are measured in dollars and corrected by flawed inflation data.

All the income figures show the same trend, that income is supposedly up by their measurements, but not at nearly the same rate as the prior quarter. For example: “Current-dollar personal income increased $65.7 billion (2.1 percent) in the third quarter, compared with an increase of $123.5 billion (4.1 percent) in the second.”

Remember, these are the first cut and we know that all these numbers will be revised downwards. The “Price Index” portion of the report supposedly rose 2.3%, this is an increase from 1.9%, and did come in above expectations of 2.0%.

Frankly, with the dollar index falling 8.4% during the quarter against a competitively devalued basket of currencies, you can see how under-reported the inflation effects are. Should they have used an 8%+ deflator, then real GDP would have been close to negative 6%! And that’s probably a lot closer to the truth. But reality is another matter entirely, as one would have to subtract out financial engineering which adds massively to “production,” yet in reality produces nothing but heartache.

Here’s Econoday’s take on the subject, it may read somewhat differently:

In a separate but related report on employment costs, we find that wages are not even close to keeping up. What does that tell you about inventory builds? This was a miss at .4%, the consensus was expecting .5%:

Note the overall slope of that chart! The bottom line for me is that we are experiencing monetary growth, while at the same time the real economy is continuing to contract. Wages are not anywhere near keeping pace with the monetary growth, this is creating the huge gaps between the top people who benefit from inflation and the bottom wage earners who suffer from it – the vast majority of people.

There is NO REASON to have an inflationary system like this! It is literally insane. It is designed to benefit the people who push debt, plain and simple. Yet, it’s absolutely possible to have a system where the government controls the production of money yet keeps the total quantity under control in such a way as to create price stability. Within that system there can still be private lending and even fractional reserves, the key is in ensuring that special interests don’t corrupt the system, again something that is completely doable given the proper TRANSPARENCY and checks and balances. There is only one inflation target that will work in the long run, that is ZERO. Targeting any other number is again quite literally insane, it is like designing your house to only last a couple of years before it falls down when you can easily design a much more solid house – we have the means and the capability to do so, all we need is the WILL to unseat those who currently possess the power of money production.

Chicago PMI and Consumer Sentiment are released shortly after the market opens, these will be reported in the daily thread.

Market divergences continue to expand, the latest is watching the VIX rise while prices stagnate. The financials are going exactly nowhere, appropriately so. Reality for them, of course, is something far worse.

Yesterday was yet another day of prices going up and down but ultimately going nowhere. All the daily candles look like top indicators. Yesterday’s action produced a very small movement again in the McClellan Oscillator, thus we can expect a large directional price move soon. Although today is not a POMO day, if I owned an HFT computer, I would most certainly program it to ramp into today’s close to front run Monday morning’s HFT ramp which will be POMO fueled in the same manner as a nitro top fueled dragster! I can almost see the flames shooting out of the headers already – especially the day prior to the elections.

What I do know is that as long as the money changers who own the HFT machines get their way, then significant declines are not likely. Once pushback occurs, then they will pull out their guns and place them to our collective heads by taking down the markets. That’s the game, it’s how it’s played. So, those very debt pushers are actually insolvent, but they exchange their crap to the “Fed” who gives them new fuel on a regular basis. Keep it coming and everything’s okay. Allow the accounting FRAUD to continue, and everything’s okay. Interrupt their game in any manner, THEN we have trouble. Watch what I’m telling you, you know it’s the truth.

And just listen to all the pushback in the political ads! Everyone is against spending more and burdening our grandkids. Laugh out loud time ten trillion! Listen, these clowns are just like all the clowns before them. They do have a part to play, however, and that part is called austerity – listen to their words. A Republican controlled Congress, they claim, is going to reel in the stimulus and excessive spending that hasn’t worked. Well guess what? That won’t work either, it will produce wave C down. But of the options within our oligarch controlled debt money system, that is the better of the two options available! Again, I can live with lower stock prices, but I can’t live without food which is going to be a problem if we attempt to inflate our way out. That’s never worked. In fact, nothing inside of a debt backed money box works for the people, it only works for the few at the top. Want proof? Okay, here it is:

Top U.S. Incomes Grew Five-Fold in 2009

There you will find that in the top income bracket measured, there are 74 people who earned more than $50 million last year. Their average income jumped last year from $91.8 million to an unbelievable $518.8 million! How are they benefiting from a system of never ending inflation? That’s a little bit different than the slope of the chart above, and this is exactly the stuff seen at the end of empires, it is the root of inequity, and it is the root of revolution. When only they can afford to eat, then history says they will be overthrown – appropriately so.

And thus the economic and political system that can stand the test of time has yet to exist on this planet. If those 74 people were smart, they’d be buying beer, corn syrup, and cable T.V. for the masses. Oh wait, 40 million plus on food stamps, that’s right, they are.

Equity futures are lower again this morning, the dollar is roughly flat, bonds are rising sharply, while oil is down slightly and gold is up.

Of course it’s pretty common knowledge that up trends typically end on good news, while downtrend end on bad news. These news events typically draw in the last rush for a given direction and produce capitulation volume. Such an event has still not happened and I think it’s very interesting how in the past couple of weeks or so the economic data has been read that if it’s bad it’s good because QE will save the world, and if it’s good it’s good. Then there are the numbers that come out EXACTLY on consensus, something that almost never happens yet there have been a string of these in the past week, this morning’s release of Q3 GDP is the latest.

Coming in exactly on consensus of 2.0% growth, look for quarter three GDP to be subsequently cut in half or more in future revisions. Q2 settled on 1.7%, and I can almost guarantee that Q3 was considerably slower than Q2. Keep in mind that GDP is measured in dollars and then “corrected” via the deflator for inflation. Again I’ll guarantee that the deflator comes nowhere near capturing the destruction that’s occurring to the dollar. Below is the entire report from the BEA:

Q3 GDP

What you will find inside that report is that inventory build resulted in the majority of the “growth,” 1.44%. Inventory builds are only good if there’s demand to buy the inventory once it’s produced. Forced inventory builds occur when goods are ordered due to miscalculations of demand. Demand is misjudged when economic data is artificial – thus bad tracking and reporting of data builds economic distortions, inventory building at this time is one.

You’ll also note in this report that almost every category tracked, while reported positive, is DECELERATING substantially from the prior report. Take exports for an example: “Real exports of goods and services increased 5.0 percent in the third quarter, compared with an increase of 9.1 percent in the second. Real imports of goods and services increased 17.4 percent, compared with an increase of 33.5 percent.” The numbers seem large, but are much smaller than the previous quarter. Again, they claim these numbers are “real,” that is adjusted for inflation, but again I have to raise the B.S. flag to full mast on those numbers. Shipping data and tax receipts do not substantiate their trade data that again are measured in dollars and corrected by flawed inflation data.

All the income figures show the same trend, that income is supposedly up by their measurements, but not at nearly the same rate as the prior quarter. For example: “Current-dollar personal income increased $65.7 billion (2.1 percent) in the third quarter, compared with an increase of $123.5 billion (4.1 percent) in the second.”

Remember, these are the first cut and we know that all these numbers will be revised downwards. The “Price Index” portion of the report supposedly rose 2.3%, this is an increase from 1.9%, and did come in above expectations of 2.0%.

Frankly, with the dollar index falling 8.4% during the quarter against a competitively devalued basket of currencies, you can see how under-reported the inflation effects are. Should they have used an 8%+ deflator, then real GDP would have been close to negative 6%! And that’s probably a lot closer to the truth. But reality is another matter entirely, as one would have to subtract out financial engineering which adds massively to “production,” yet in reality produces nothing but heartache.

Here’s Econoday’s take on the subject, it may read somewhat differently:

Highlights

The recovery regained incremental strength in the third quarter, but the pace is still quite soft. Third quarter GDP expanded at a 2.0 percent annualized pace, following a 1.7 percent rise the prior quarter. The latest figure matched analysts' projections for a 2.0 percent gain.

The latest quarter was led by gains in inventory investment, consumer spending, equipment investment, and government purchases. On the negative side, housing investment fell back and net exports worsened on higher imports. Exports rose moderately.

How strong final sales are is still an important issue in terms of whether demand is picking up or not and it slowed by both key measures. Growth in real final sales to domestic purchasers slowed to 2.5 percent, following a 4.3 percent boost in the second quarter. Final sales of domestic product (adds in net exports) eased to 0.6 percent from 0.9 percent annualized in the second quarter. A big question is whether the boost in imports reflects optimism on the part of businesses that spending is going to pick up-and there is no certain answer. The surge in both imports and inventories at the same time implies optimism. But if demand does not pick up, the boost in inventories will be a negative in coming quarters.

Year-on-year, real GDP in the second quarter is up 3.1 percent, compared 3.0 percent in the second quarter.

Economy-wide inflation as measured by the GDP price index firmed to 2.3 percent in the third quarter, following a 1.9 percent increase the previous period. The median market forecast was for a 2.0 percent rise.

In a separate but related report on employment costs, we find that wages are not even close to keeping up. What does that tell you about inventory builds? This was a miss at .4%, the consensus was expecting .5%:

Highlights

A slowdown in wages & salaries made for a slowdown in the third-quarter employment cost index, at plus 0.4 percent vs. the second-quarter's plus 0.5 percent. The on-year rate is plus 1.9 percent vs plus 1.8 percent in the second quarter. Wages & salaries rose only 0.3 percent in the third quarter, down from the second-quarter's 0.4 percent. The on-year rate slipped one tenth to plus 1.5 percent, a rate just above on-year consumer price inflation which has been trending slightly over 1.0 percent. Benefit costs were unchanged at 0.6 percent though the on-year rate rose two tenths from the second quarter to plus 2.7 percent. Employment costs remain very quiet, giving the Federal Reserve the leeway it needs for further accommodation.

Note the overall slope of that chart! The bottom line for me is that we are experiencing monetary growth, while at the same time the real economy is continuing to contract. Wages are not anywhere near keeping pace with the monetary growth, this is creating the huge gaps between the top people who benefit from inflation and the bottom wage earners who suffer from it – the vast majority of people.

There is NO REASON to have an inflationary system like this! It is literally insane. It is designed to benefit the people who push debt, plain and simple. Yet, it’s absolutely possible to have a system where the government controls the production of money yet keeps the total quantity under control in such a way as to create price stability. Within that system there can still be private lending and even fractional reserves, the key is in ensuring that special interests don’t corrupt the system, again something that is completely doable given the proper TRANSPARENCY and checks and balances. There is only one inflation target that will work in the long run, that is ZERO. Targeting any other number is again quite literally insane, it is like designing your house to only last a couple of years before it falls down when you can easily design a much more solid house – we have the means and the capability to do so, all we need is the WILL to unseat those who currently possess the power of money production.

Chicago PMI and Consumer Sentiment are released shortly after the market opens, these will be reported in the daily thread.

Market divergences continue to expand, the latest is watching the VIX rise while prices stagnate. The financials are going exactly nowhere, appropriately so. Reality for them, of course, is something far worse.

Yesterday was yet another day of prices going up and down but ultimately going nowhere. All the daily candles look like top indicators. Yesterday’s action produced a very small movement again in the McClellan Oscillator, thus we can expect a large directional price move soon. Although today is not a POMO day, if I owned an HFT computer, I would most certainly program it to ramp into today’s close to front run Monday morning’s HFT ramp which will be POMO fueled in the same manner as a nitro top fueled dragster! I can almost see the flames shooting out of the headers already – especially the day prior to the elections.

What I do know is that as long as the money changers who own the HFT machines get their way, then significant declines are not likely. Once pushback occurs, then they will pull out their guns and place them to our collective heads by taking down the markets. That’s the game, it’s how it’s played. So, those very debt pushers are actually insolvent, but they exchange their crap to the “Fed” who gives them new fuel on a regular basis. Keep it coming and everything’s okay. Allow the accounting FRAUD to continue, and everything’s okay. Interrupt their game in any manner, THEN we have trouble. Watch what I’m telling you, you know it’s the truth.

And just listen to all the pushback in the political ads! Everyone is against spending more and burdening our grandkids. Laugh out loud time ten trillion! Listen, these clowns are just like all the clowns before them. They do have a part to play, however, and that part is called austerity – listen to their words. A Republican controlled Congress, they claim, is going to reel in the stimulus and excessive spending that hasn’t worked. Well guess what? That won’t work either, it will produce wave C down. But of the options within our oligarch controlled debt money system, that is the better of the two options available! Again, I can live with lower stock prices, but I can’t live without food which is going to be a problem if we attempt to inflate our way out. That’s never worked. In fact, nothing inside of a debt backed money box works for the people, it only works for the few at the top. Want proof? Okay, here it is:

Top U.S. Incomes Grew Five-Fold in 2009

There you will find that in the top income bracket measured, there are 74 people who earned more than $50 million last year. Their average income jumped last year from $91.8 million to an unbelievable $518.8 million! How are they benefiting from a system of never ending inflation? That’s a little bit different than the slope of the chart above, and this is exactly the stuff seen at the end of empires, it is the root of inequity, and it is the root of revolution. When only they can afford to eat, then history says they will be overthrown – appropriately so.

And thus the economic and political system that can stand the test of time has yet to exist on this planet. If those 74 people were smart, they’d be buying beer, corn syrup, and cable T.V. for the masses. Oh wait, 40 million plus on food stamps, that’s right, they are.

Morning Update/ Market Thread 10/28

Good Morning,

Equity futures are higher this morning with the dollar plummeting, bonds flat, oil and gold higher.

The “shocking” news this morning for those who don’t understand the real power structure of the United States, is that the “Fed” is asking the Primary Dealers for input in regards to size and timing of QE2. This is no shock at all, of course, for those who understand that the Primary Dealers OWN the “Fed” quite literally. The only shock to me regarding this insight is that they are saying so publically. And here’s the Emperor is wearing no clothes part… this means that they have no idea how big it should be and yet the market already has $____??? priced in! Naturally, if you are a bank, how big and how often do you think you want QE to be? Does that worry you?

THE FED IS THE PROBLEM! What’s most important is WHO is in control of your money – clearly it is not the people, nor is it Congress or anyone else who is actually an elected representative.

And you know what scares me far more than a crashing stock market? One that melts up directly into hyperinflation – that scares the hell out of me. It would very quickly lead to a loss of confidence and would make it extremely difficult for most people to live. You can live with low priced stock, but you cannot live without food.

But we certainly know who is not going to be living without… that would be Exxon Mobile who just announced profits increased 55% and that they earned only a pitiful $7.35 Billion in the 3rd quarter! LOL, might as well just start talking about profits in the trillions because at the rate our money is going it won’t be long. Yes, they pin this on the higher price of oil… dollar down, things priced in dollars up, thus “profits” go up for everything priced in dollars. In other words, it’s an illusion, and a quite nasty one at that as last time I checked my income was not increasing at anywhere near that type of pace, and I’ll wager my “vast fortune” that yours aren’t either.

And it’s time to put on the party hats, because the weekly Jobless Claims fell below 450k to “only” 434,000 wretched souls. Naturally the week prior was revised higher by the population of only a small town, and therefore I guess we should be thankful the revision wasn’t the size of a small city. Here’s Econospin:

Once again take a look at the chart, this is still in the same sideways range we’ve been in for months and months. Anything over 350k is a complete disaster and indicates that we’re still losing jobs like crazy, we are not creating them, and we are certainly not keeping up with the growth rate of our population. And on an unadjusted bases, claims for the prior week actually INCREASED by 11,678 people. The other bad news that will be interpreted as good is that those drawing Emergency Unemployment dropped by a very large 258k, plunging the number who receive this compensation well below the 4 million mark. This is a double edged sword as it means tens of thousands of people are running out of benefits – what happens to them now? Get ready to spend more on prisons, as desperate people do desperate things… but then again, there’s nothing like a hungry citizenry to bring about CHANGE. The oligarchs had better get busy with their next population placation, they are starting to fall behind.

Did I mention that I'm moving out of "the hot zone" and into the small town where I grew up and consider to be more safe? Karma being what it is, I'll probably get mugged in the world class park just down the street. Should this occur, please send donations to Children's Hospital in lieu of flowers, thanks.

Yesterday produced yet another hammer in the markets – one topping candlestick after the other. What’s priced in? Who’s on first? It’s all B.S., yesterday afternoon prices did yet another HFT zoom to front-run today’s nitro fueled POMO. So what’s the POMO exit strategy? Is there one? Perhaps we should ask the Primary Dealers?

And Zero Hedge reports that the Japanese have announced they are going to monetize ETFs, REITs, as well as BBB and higher rated bonds. According to them:

Yes, the central banks of the world buying ETFs out in the open, now it’s officially nuts! Again I ask, “What is their exit strategy?” Do they plan on owning them forever? And so it doesn’t take a genius imagination to project how this ends. Badly seems to sum it up in just one word. Again, we knew that wild stuff, unimagined stuff, was going to happen, yet it seems surreal to actually watch the disaster unfold. If I walked up to you 5 years ago and said that the central bank of Japan was going to be buying up ETF’s, you would have laughed… and here we are. Of course 5 years ago I was saying that our money system was going to end and that it was going to be a wild ride getting there. And so we know the destination is the destruction of our money system, but the way in which we get there is not under our control, it’s under the control of those who profit from the creation of inflation – they are quite literally insane, every decision they make has been for THEIR benefit at the often life threatening expense of others. And that’s the very definition of narcissism, the result of failing to maintain control of the production of money by the people. Here, would you like to see the path of your money? Here it is, just the past 20 hours or so… another 1.06% gone in less than a day.

So, on one hand every piece of data or news that can be interpreted as “improvement” is hailed, but at the same time the economy sucks so bad that the banks must do trillion dollar QEs and directly buy up risk assets. Does any of that add up? Again, what’s the exit strategy? And for the nuts of the world who think that the central banks are doing us a favor (there are many), I can only say that a fool and their money are soon parted.

I think I’ll go buy some gold…

The Rolling Stones : Sympathy For The Devil:

Equity futures are higher this morning with the dollar plummeting, bonds flat, oil and gold higher.

The “shocking” news this morning for those who don’t understand the real power structure of the United States, is that the “Fed” is asking the Primary Dealers for input in regards to size and timing of QE2. This is no shock at all, of course, for those who understand that the Primary Dealers OWN the “Fed” quite literally. The only shock to me regarding this insight is that they are saying so publically. And here’s the Emperor is wearing no clothes part… this means that they have no idea how big it should be and yet the market already has $____??? priced in! Naturally, if you are a bank, how big and how often do you think you want QE to be? Does that worry you?

Fed Asks Dealers to Estimate Size of Debt Purchases

Oct. 28 (Bloomberg) -- The Federal Reserve asked bond dealers and investors for projections of central bank asset purchases over the next six months, along with the likely effect on yields, as it seeks to gauge the possible impact of new efforts to spur growth.

The New York Fed survey, obtained by Bloomberg News, asks about expectations for the initial size of any new program of debt purchases and the time over which it would be completed. It also asks firms how often they anticipate the Fed will re- evaluate the program, and to estimate its ultimate size.

With their benchmark interest rate near zero, policy makers meet Nov. 2-3 to consider steps to boost an economy that’s growing too slowly to reduce unemployment near a 26-year high. Financial-market participants are focusing on the size, timing and maturities of likely purchases aimed at lowering long-term rates, with estimates reaching $1 trillion or more.

“If they buy too much, I think there’s a real chance that rates are going to rise because people are worried about inflation,” said Stephen Stanley, chief economist at Pierpont Securities LLC in Stamford, Connecticut. “If they don’t buy much, they’re not going to have a market impact.”

THE FED IS THE PROBLEM! What’s most important is WHO is in control of your money – clearly it is not the people, nor is it Congress or anyone else who is actually an elected representative.

And you know what scares me far more than a crashing stock market? One that melts up directly into hyperinflation – that scares the hell out of me. It would very quickly lead to a loss of confidence and would make it extremely difficult for most people to live. You can live with low priced stock, but you cannot live without food.

But we certainly know who is not going to be living without… that would be Exxon Mobile who just announced profits increased 55% and that they earned only a pitiful $7.35 Billion in the 3rd quarter! LOL, might as well just start talking about profits in the trillions because at the rate our money is going it won’t be long. Yes, they pin this on the higher price of oil… dollar down, things priced in dollars up, thus “profits” go up for everything priced in dollars. In other words, it’s an illusion, and a quite nasty one at that as last time I checked my income was not increasing at anywhere near that type of pace, and I’ll wager my “vast fortune” that yours aren’t either.

And it’s time to put on the party hats, because the weekly Jobless Claims fell below 450k to “only” 434,000 wretched souls. Naturally the week prior was revised higher by the population of only a small town, and therefore I guess we should be thankful the revision wasn’t the size of a small city. Here’s Econospin:

Highlights

Claims data offer rare good news on the labor market as initial claims fell steeply to 434,000 in an October 23 week that isn't skewed by special factors. The level is the lowest since July as is the four-week average of 453,250. Given that July's data were distorted by adjustment problems tied to auto retooling, the latest batch of data is perhaps the best so far of the recovery.

Continuing claims for the October 16 week fell 122,000 to a two-year low of 4.356 million. The four-week average of 4.447 million is down 39,000. The unemployment rate for insured workers slipped one tenth to 3.5 percent. Emergency claims and those on extended benefits are also down.

Once again take a look at the chart, this is still in the same sideways range we’ve been in for months and months. Anything over 350k is a complete disaster and indicates that we’re still losing jobs like crazy, we are not creating them, and we are certainly not keeping up with the growth rate of our population. And on an unadjusted bases, claims for the prior week actually INCREASED by 11,678 people. The other bad news that will be interpreted as good is that those drawing Emergency Unemployment dropped by a very large 258k, plunging the number who receive this compensation well below the 4 million mark. This is a double edged sword as it means tens of thousands of people are running out of benefits – what happens to them now? Get ready to spend more on prisons, as desperate people do desperate things… but then again, there’s nothing like a hungry citizenry to bring about CHANGE. The oligarchs had better get busy with their next population placation, they are starting to fall behind.

Did I mention that I'm moving out of "the hot zone" and into the small town where I grew up and consider to be more safe? Karma being what it is, I'll probably get mugged in the world class park just down the street. Should this occur, please send donations to Children's Hospital in lieu of flowers, thanks.

Yesterday produced yet another hammer in the markets – one topping candlestick after the other. What’s priced in? Who’s on first? It’s all B.S., yesterday afternoon prices did yet another HFT zoom to front-run today’s nitro fueled POMO. So what’s the POMO exit strategy? Is there one? Perhaps we should ask the Primary Dealers?

And Zero Hedge reports that the Japanese have announced they are going to monetize ETFs, REITs, as well as BBB and higher rated bonds. According to them:

In other words, the BOJ is now permitted to do what the Fed will have authority to do with a few months: buy virtually all risk assets, as buying ETFs is the same as buying the general market courtesy of the most traded security in the world, SPY, to push and pull the entire market in whatever direction it goes. There are two questions at this point: is the BOJ allowed to buy foreign (read US) assets that fall under the above buckets, and whether the FX currency swap line recently established with the BOJ will allow the Fed to use Japanese proxies to monetize various US assets. Or will the Fed first seek input from the BOJ on how to proceed with sending the Dow to 36k.

Yes, the central banks of the world buying ETFs out in the open, now it’s officially nuts! Again I ask, “What is their exit strategy?” Do they plan on owning them forever? And so it doesn’t take a genius imagination to project how this ends. Badly seems to sum it up in just one word. Again, we knew that wild stuff, unimagined stuff, was going to happen, yet it seems surreal to actually watch the disaster unfold. If I walked up to you 5 years ago and said that the central bank of Japan was going to be buying up ETF’s, you would have laughed… and here we are. Of course 5 years ago I was saying that our money system was going to end and that it was going to be a wild ride getting there. And so we know the destination is the destruction of our money system, but the way in which we get there is not under our control, it’s under the control of those who profit from the creation of inflation – they are quite literally insane, every decision they make has been for THEIR benefit at the often life threatening expense of others. And that’s the very definition of narcissism, the result of failing to maintain control of the production of money by the people. Here, would you like to see the path of your money? Here it is, just the past 20 hours or so… another 1.06% gone in less than a day.

So, on one hand every piece of data or news that can be interpreted as “improvement” is hailed, but at the same time the economy sucks so bad that the banks must do trillion dollar QEs and directly buy up risk assets. Does any of that add up? Again, what’s the exit strategy? And for the nuts of the world who think that the central banks are doing us a favor (there are many), I can only say that a fool and their money are soon parted.

I think I’ll go buy some gold…

The Rolling Stones : Sympathy For The Devil:

Morning Update/ Market Thread 10/27

Good Morning,

Equities are lower this morning with the dollar up, bonds down significantly more, and both oil and gold down.

So, here we are less than a week away from elections that will take away Obama’s magic shield of overwhelming Congressional power, and the whole world is expecting QE 2 to the tune of $100 billion per month! $100 billion per month! And what has got to worry the bejeezus out of the oligarchs is the fact that bonds are sliding hard in price sending interest rates for their “assets” (debt) up! The breakdown of the long bond is quite disturbing if you understand that the goal of QE is to keep it moving in the opposite direction:

A breakdown below support at the 129 level on that chart will signify further breakdown. Yes, bonds are in a bubble, and it is massive. Just think about all the people, now deathly and appropriately afraid of stocks who have rushed into bonds… perfect timing, just in time for them to buy into what will prove to be the last bubble. They got suckered into stocks, then into buying multiple homes, and now bonds.

And what’s so frightening at this juncture is that the likes of Bernanke believes that they can keep rates low via money creation! The truth is the exact opposite! The more they QE, the HIGHER rates will eventually go! There is no fooling the math of debt, ALL debts get repaid with interest in one way or the other. Attempting to fool the math will only lead to either higher rates or to a falling value of our currency. Failing to recognize and respect this fact will lead only to larger and larger attempts to stop it.

Of course assuming that they (the oligarchs) don’t recognize what’s occurring is simply naïve. The people of this country must realize that they are being DELIBERATELY robbed of their futures, and when they do then hopefully they can work to unseat the illegitimate oligarchic organizations of the globe, namely the “Fed,” IMF, BIS, CFR, and even the subordinate organizations like the United Nations whose existence is a good idea in concept, but in practice they have been bought off and controlled by the people inside the global money changing cartel.

That’s a critically important to paragraph to understand. It is these people who are butchering the rule of law, and it is up to the people to reinstate the rule of law. Step one in doing so is to prosecute their crimes and to throw those responsible in prison. THEN we can get on with the business of reestablishing a money system that works, and we can work to fairly and equitably resolve the debt saturation problem those debt pushing fraudsters created.

Other than that I have no strong opinions!

The morally bankrupt, hypocritical, and corrupt Mortgage Banker’s Association released their worthless and intentionally deceiving Purchase Applications for the prior week – here’s Econoday:

Stabilizing? What nonsense. And what a worthless set of data, the MBA refuses to give out hard numbers of anything. That’s simply because they want to deceive and spin their web of lies by only using weekly percentages – it’s a simple game that attempts to fool the weak minded.

Durable Goods orders increased a large 3.3% in the past month – this is well above last month’s -1.3% decline, and it is more than the +1.6% consensus. However, the increase was almost entirely based upon aircraft orders, and with those removed, Durable Goods orders actually fell .8%.

With my experience in the Airline industry, I can tell you that airlines are notoriously bad at timing aircraft orders. In fact, they generally buy exactly when they shouldn’t be, and are not buying exactly when they should be. Of course this is because they are victims of the credit cycle created by the mobsters who run our nation. And the lead times necessary in the order process set up a P.I.O. (pilot induced oscillation) that puts them out of synch with the real economy. In other words, their passenger loads are high right now, and so they are ordering again, but that is likely to change before they actually take delivery of the aircraft they are ordering now.

And what do airliners depend upon? Oil of course! And thus I thought this little tidbit this morning was very interesting for those who understand the concept of peak oil:

My oh my – that’s a game changer if it’s true and not just disinformation. Hard to know in today’s world as every release must not be taken at face value. What agenda and motivation does the Geological Survey have in generating this release, and what political influence are they under? That I don’t know, but this would throw a large wrinkle at those who think Alaska is going to make the U.S. anywhere close to energy independent anytime soon.

New Home Sales are released at 10 Eastern this morning.

Yet another gap on the open today. No POMO today, but there will be tomorrow and then again this coming Monday.

Yesterday the market produced a hammer and wound up essentially where it started. This again “coils the spring” in anticipation of a large directional move. Again the McClellan (spelled correctly this time) Oscillator turned negative. The prior day’s shooting star/ gravestone doji contrasts with yesterday’s hammer to produce what I call “dueling hammers.” Dueling hammers are almost always resolved with prices moving in the direction of the handle of the most recent hammer – in this case that would be down, and that’s what the opening is producing. Regardless, these are all topping candlesticks, of which there have been many. The technical divergences are roaring about a top! And yet here we are, simply going nowhere while we await our executioner – what will it be? Death by a hundred billion per month, or should we just blast our own brains out with a couple of trillion right up front? Personally, I would prefer to die quickly than to be tortured to death by the likes of Fedspeak and the trickle of poison that the debt pushers prefer.

Equities are lower this morning with the dollar up, bonds down significantly more, and both oil and gold down.

So, here we are less than a week away from elections that will take away Obama’s magic shield of overwhelming Congressional power, and the whole world is expecting QE 2 to the tune of $100 billion per month! $100 billion per month! And what has got to worry the bejeezus out of the oligarchs is the fact that bonds are sliding hard in price sending interest rates for their “assets” (debt) up! The breakdown of the long bond is quite disturbing if you understand that the goal of QE is to keep it moving in the opposite direction:

A breakdown below support at the 129 level on that chart will signify further breakdown. Yes, bonds are in a bubble, and it is massive. Just think about all the people, now deathly and appropriately afraid of stocks who have rushed into bonds… perfect timing, just in time for them to buy into what will prove to be the last bubble. They got suckered into stocks, then into buying multiple homes, and now bonds.

And what’s so frightening at this juncture is that the likes of Bernanke believes that they can keep rates low via money creation! The truth is the exact opposite! The more they QE, the HIGHER rates will eventually go! There is no fooling the math of debt, ALL debts get repaid with interest in one way or the other. Attempting to fool the math will only lead to either higher rates or to a falling value of our currency. Failing to recognize and respect this fact will lead only to larger and larger attempts to stop it.

Of course assuming that they (the oligarchs) don’t recognize what’s occurring is simply naïve. The people of this country must realize that they are being DELIBERATELY robbed of their futures, and when they do then hopefully they can work to unseat the illegitimate oligarchic organizations of the globe, namely the “Fed,” IMF, BIS, CFR, and even the subordinate organizations like the United Nations whose existence is a good idea in concept, but in practice they have been bought off and controlled by the people inside the global money changing cartel.

That’s a critically important to paragraph to understand. It is these people who are butchering the rule of law, and it is up to the people to reinstate the rule of law. Step one in doing so is to prosecute their crimes and to throw those responsible in prison. THEN we can get on with the business of reestablishing a money system that works, and we can work to fairly and equitably resolve the debt saturation problem those debt pushing fraudsters created.

Other than that I have no strong opinions!

The morally bankrupt, hypocritical, and corrupt Mortgage Banker’s Association released their worthless and intentionally deceiving Purchase Applications for the prior week – here’s Econoday:

Highlights

The volume of purchase applications picked up after two weeks of steep declines, 3.9 percent higher in the October 22 week. Refinancing applications rose 3.0 percent. The gains coincide with a drop in mortgage rates including a nine basis point decline for 30-year loans to 4.25 percent. This week's heavy run of housing data indicates the sector is stabilizing at a very low level.

Stabilizing? What nonsense. And what a worthless set of data, the MBA refuses to give out hard numbers of anything. That’s simply because they want to deceive and spin their web of lies by only using weekly percentages – it’s a simple game that attempts to fool the weak minded.

Durable Goods orders increased a large 3.3% in the past month – this is well above last month’s -1.3% decline, and it is more than the +1.6% consensus. However, the increase was almost entirely based upon aircraft orders, and with those removed, Durable Goods orders actually fell .8%.

Highlights

Aircraft orders lifted overall durables sharply in September but ex-transportation components are mixed and net down. New factory orders for durable goods in September rebounded 3.3 percent, following a 1.0 percent decrease in August. The gain in September came in significantly above the consensus forecast for a 1.6 percent boost. Excluding transportation, new durables orders fell back 0.8 percent, following a 1.9 percent increase in August.

By major industries, transportation led orders up, jumping 15.7 percent in September after declining 8.8 percent the prior month. Nondefense aircraft soared a monthly 105.0 percent after dropping 30.0 percent the month before. Defense aircraft orders advanced 30.0 percent in September while motor vehicles slipped 0.4 percent.

Other components were mixed but more down than up. Declines were seen in primary metals, down 0.5 percent; fabricated metals, down 1.6 percent; computers & electronics, down 4.0 percent; communications equipment, down 18.6 percent; and "all other," down 0.1 percent. Gains were seen in machinery, up 2.0 percent, and in electrical equipment, up 0.4 percent.

Business investment in equipment continues to oscillate between positives and negatives due to its inherent monthly volatility and only moderate uptrend. Nondefense capital goods orders excluding aircraft in September slipped 0.6 percent after jumping 4.8 percent in August. Shipments for this series continued to edge up, rising 0.4 percent in September after gaining 1.3 percent the prior month.

Year-on-year, overall new orders for durable goods in September held steady at up 12.2 percent. Excluding transportation, new durables orders eased to up 9.5 percent from 13.6 percent the prior month.

The bottom line is that durables excluding transportation have been typically volatile but essentially flat over the last few months. Growth in manufacturing appears to be slowing at least for the near term. On the news, equity futures declined marginally while Treasury rates were little changed.

With my experience in the Airline industry, I can tell you that airlines are notoriously bad at timing aircraft orders. In fact, they generally buy exactly when they shouldn’t be, and are not buying exactly when they should be. Of course this is because they are victims of the credit cycle created by the mobsters who run our nation. And the lead times necessary in the order process set up a P.I.O. (pilot induced oscillation) that puts them out of synch with the real economy. In other words, their passenger loads are high right now, and so they are ordering again, but that is likely to change before they actually take delivery of the aircraft they are ordering now.

And what do airliners depend upon? Oil of course! And thus I thought this little tidbit this morning was very interesting for those who understand the concept of peak oil:

Alaska's untapped oil reserves estimate lowered 90 percent

The U.S. Geological Survey says a revised estimate for the amount of conventional, undiscovered oil in the National Petroleum Reserve in Alaska is a fraction of a previous estimate.

The group estimates about 896 million barrels of such oil are in the reserve, about 90 percent less than a 2002 estimate of 10.6 billion barrels.

The new estimate is mainly due to the incorporation of new data from recent exploration drilling revealing gas occurrence rather than oil in much of the area, the geological survey said.

My oh my – that’s a game changer if it’s true and not just disinformation. Hard to know in today’s world as every release must not be taken at face value. What agenda and motivation does the Geological Survey have in generating this release, and what political influence are they under? That I don’t know, but this would throw a large wrinkle at those who think Alaska is going to make the U.S. anywhere close to energy independent anytime soon.

New Home Sales are released at 10 Eastern this morning.

Yet another gap on the open today. No POMO today, but there will be tomorrow and then again this coming Monday.

Yesterday the market produced a hammer and wound up essentially where it started. This again “coils the spring” in anticipation of a large directional move. Again the McClellan (spelled correctly this time) Oscillator turned negative. The prior day’s shooting star/ gravestone doji contrasts with yesterday’s hammer to produce what I call “dueling hammers.” Dueling hammers are almost always resolved with prices moving in the direction of the handle of the most recent hammer – in this case that would be down, and that’s what the opening is producing. Regardless, these are all topping candlesticks, of which there have been many. The technical divergences are roaring about a top! And yet here we are, simply going nowhere while we await our executioner – what will it be? Death by a hundred billion per month, or should we just blast our own brains out with a couple of trillion right up front? Personally, I would prefer to die quickly than to be tortured to death by the likes of Fedspeak and the trickle of poison that the debt pushers prefer.

Morning Update/ Market Thread 10/26

Good Morning,

Equity futures are lower this morning, the dollar is stronger, but bonds are significantly weaker. Oil and gold are both lower.

Yesterday’s run higher was extremely weak and faded late day to produce topping tail type candlesticks. Volume was the second lowest of the year! That’s not something you want to see with a new high attempt if you’re a bull. The Transports did make a new intraday high above the April high, but the Industrials did not – closing highs are what matter most for DOW Theory.

The up/down action caused yet another small movement in the McClellan Oscillator and so we can expect a large price move soon – the McClellan did finish in barely positive territory. Yesterday was another Bradley Model turn date – these have been run over lately but we are certainly past due for a trend change.

But we can’t have any of that in front of an election, now can we? Oh no… so therefore today is another POMO, as is Thursday. Thus you can expect rising prices to come out of nowhere as the POMO operation begins - only to have all that money vaporize later. So, don’t be surprised to see what was clearly a topping candlestick get overrun by brute stupidity. Following the POMO on Thursday, of course, we will naturally want to Pavlov higher Friday afternoon to get in front of the Monday morning ramp job which should be a doozy as there’s another POMO scheduled for Monday, the day prior to the election! Oh yeah, that’ll be nice… or because everyone knows the game thoroughly now the reversal happens now. Whatever steals the most money... personally I don’t have a supercomputer to figure it out, but we know the large banks do. And that really makes a mere mortal playing their game a fool.

Meanwhile the historic divergences continue to grow, saying to me that the reversal when it comes is going to shock a lot of people.

There’s quite a bit of data coming out this morning, unfortunately most of it comes later after the open. The Case-Shiller Home Price Index comes out at 9 Eastern. Consumer Confidence, the FHFA House Price Index, Richmond Fed, and State Street Investor Confidence are all released at 10 Eastern. We will report on these results in the daily thread.

You can see in the 30 minute chart of the SPX below that we are creating a megaphone top formation. Megaphones typically reverse the trend going into them:

Yesterday the VIX was positive at the same time the markets were positive. This is another sign that people (are there any humans left?) are positioning themselves for a trend change:

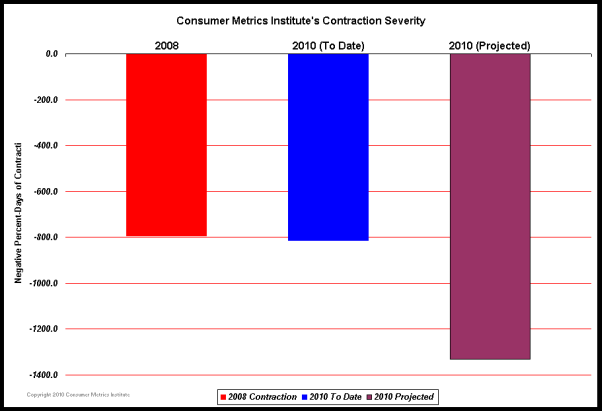

Yesterday the Consumer Metrics Institute released a report saying that the real economic contraction of 2010 now exceeds the contraction of 2008! And it’s forecast to FAR exceed the contraction of 2008. Is that what the mainstream media and government statistics are telling you?

Comstock Funds posted a good chart recently showing where we are in the deflation cycle. I think this chart is excellent. What it is saying is basically that wave C of the deflationary wave is still coming:

Of course the market is going to gap lower at the open. Every day begins with a gap in HFT land. That way they can get in front of any real humans left and reverse the trade once they have suckered said human into a trade. They see the human’s bid even before it is executed, and then they see whatever stop is inserted as well. There are so few humans left willing to play this game, however, that WHEN the owners of the HFTs turn their machines off, the market is going to instantly (as in a flash) go no bid. It’s generally a really terrific way to build a market and to inspire confidence.

Speaking of inspiring confidence, the asshat award of the month goes to Warren Buffett’s Berkshire Hathaway:

And there you have someone who once again clearly believes they are above the rule of law while they march along their merry way producing nothing but ACCOUNTING FRAUD. And this is the game that our entire economy is built upon. Earnings beats? LOL, nothing but fraud. And that’s the story of the failure of this current Administration, isn’t it? They have failed to uphold the rule of law. No convictions, no prison time, no enforcement of the rule of law. How important is it? It is nation ending important.

When you see the rule of law being enforced, THEN will be the time to start getting serious again about “investing.” Until then, it’s all fraud all the time. I’ll go long the market in earnest the day that Warren Buffett is behind bars sharing a cell with the likes of Dimon and Paulson – I don’t think I’ll hold my breath waiting.

Pink Floyd- Pigs On The Wing:

Equity futures are lower this morning, the dollar is stronger, but bonds are significantly weaker. Oil and gold are both lower.

Yesterday’s run higher was extremely weak and faded late day to produce topping tail type candlesticks. Volume was the second lowest of the year! That’s not something you want to see with a new high attempt if you’re a bull. The Transports did make a new intraday high above the April high, but the Industrials did not – closing highs are what matter most for DOW Theory.

The up/down action caused yet another small movement in the McClellan Oscillator and so we can expect a large price move soon – the McClellan did finish in barely positive territory. Yesterday was another Bradley Model turn date – these have been run over lately but we are certainly past due for a trend change.

But we can’t have any of that in front of an election, now can we? Oh no… so therefore today is another POMO, as is Thursday. Thus you can expect rising prices to come out of nowhere as the POMO operation begins - only to have all that money vaporize later. So, don’t be surprised to see what was clearly a topping candlestick get overrun by brute stupidity. Following the POMO on Thursday, of course, we will naturally want to Pavlov higher Friday afternoon to get in front of the Monday morning ramp job which should be a doozy as there’s another POMO scheduled for Monday, the day prior to the election! Oh yeah, that’ll be nice… or because everyone knows the game thoroughly now the reversal happens now. Whatever steals the most money... personally I don’t have a supercomputer to figure it out, but we know the large banks do. And that really makes a mere mortal playing their game a fool.

Meanwhile the historic divergences continue to grow, saying to me that the reversal when it comes is going to shock a lot of people.

There’s quite a bit of data coming out this morning, unfortunately most of it comes later after the open. The Case-Shiller Home Price Index comes out at 9 Eastern. Consumer Confidence, the FHFA House Price Index, Richmond Fed, and State Street Investor Confidence are all released at 10 Eastern. We will report on these results in the daily thread.

You can see in the 30 minute chart of the SPX below that we are creating a megaphone top formation. Megaphones typically reverse the trend going into them:

Yesterday the VIX was positive at the same time the markets were positive. This is another sign that people (are there any humans left?) are positioning themselves for a trend change:

Yesterday the Consumer Metrics Institute released a report saying that the real economic contraction of 2010 now exceeds the contraction of 2008! And it’s forecast to FAR exceed the contraction of 2008. Is that what the mainstream media and government statistics are telling you?

Comstock Funds posted a good chart recently showing where we are in the deflation cycle. I think this chart is excellent. What it is saying is basically that wave C of the deflationary wave is still coming:

Of course the market is going to gap lower at the open. Every day begins with a gap in HFT land. That way they can get in front of any real humans left and reverse the trade once they have suckered said human into a trade. They see the human’s bid even before it is executed, and then they see whatever stop is inserted as well. There are so few humans left willing to play this game, however, that WHEN the owners of the HFTs turn their machines off, the market is going to instantly (as in a flash) go no bid. It’s generally a really terrific way to build a market and to inspire confidence.

Speaking of inspiring confidence, the asshat award of the month goes to Warren Buffett’s Berkshire Hathaway:

Berkshire Hathaway Tells SEC: Accounting Rules Don't Apply To Us, And We Don't Have To Take Writedowns

Is Berkshire Hathaway asking the SEC for special treatment?

The regulator questioned Buffett's firm in May over a glaring absence in write-downs concerning losses worth $1.86 billion on Kraft and US Bancorp, Reuters reported today.

Berkshire denies any accounting malpractice despite the fact that the losses endured for at least 12 months and were clearly not temporary under SEC guidelines.

Here's what Berkshire CFO Marc Hamburg wrote in a response letter (which can be viewed in full at Zero Hedge) to the SEC's queries in May:We believe it is reasonably possible that the market prices of Kraft Foods and U.S. Bancorp will recover to our cost within the next one to two years assuming that there are no material adverse events affecting these companies or the industries in which they operate.Hamburg then attempts to further justify Berkshire's actions by arguing that the firm is pretty sure the losses are "recoverable through anticipated future investment income" (ok...) and that the firm has a talent for holding securities for long periods of time, so it can wait for the shares to bounce back (hmmm).

We believe that our conclusions to not record other-than-temporary impairment charges on investments in an unrealized loss position for more than twelve consecutive months was appropriate and in accordance with ASC 320 and Topic 5M.

And there you have someone who once again clearly believes they are above the rule of law while they march along their merry way producing nothing but ACCOUNTING FRAUD. And this is the game that our entire economy is built upon. Earnings beats? LOL, nothing but fraud. And that’s the story of the failure of this current Administration, isn’t it? They have failed to uphold the rule of law. No convictions, no prison time, no enforcement of the rule of law. How important is it? It is nation ending important.

When you see the rule of law being enforced, THEN will be the time to start getting serious again about “investing.” Until then, it’s all fraud all the time. I’ll go long the market in earnest the day that Warren Buffett is behind bars sharing a cell with the likes of Dimon and Paulson – I don’t think I’ll hold my breath waiting.

Pink Floyd- Pigs On The Wing:

Bill Black on Dylan Ratigan – “Fire Holder, Geithner, and Bernanke!”

More from Dylan and especially Bill Black who tells it like it is like no other – “Fire Holder, Geithner, Bernanke, and enforce the rule of law!” Amen to that, and what he is most adept at is pinning the blame where it belongs – on the banks! (Black begins about 5:10 in)

Morning Update/ Market Thread 10/25

Good Morning,

It’s a Monday... so naturally equity futures have been ramped higher on the back of a dollar that is being crushed. Bonds are soaring higher in a schizoid quantitative fit, the Yen is reaching new completely out of order heights, Oil is reaching for $83 a barrel, and gold is climbing again evidently leaving its mini-correction behind.

And just look at all the manipulation that occurs when you put the G20 together for a weekend! Oh yeah, the IMF “good guys” are going to reorganize to give more power to the emerging markets and they are going to open up its membership to “voting.” LOL, AS IF they are even some type of legitimate organization, THEY ARE NOT, they have as much legal basis as MERS (none), and the U.S.’s participation with the DEBT PUSHING CRIMINALS is not sanctioned by the people of the United States. Giving more power to “emerging markets” is telling us loud and clear that means LESS POWER for the United States! It means the oligarchy who are robbing America blind (same people who own the big banks here, they own the Fed, they own the politicians, they own the exchanges, they own the HFT computers, they own the media, and they own the military industrial complex!!!), are simply packing up their U.S. operations (as we are now debt saturated) and they are moving to take advantage of the next group of as of yet unsaturated saps who have yet to learn better.

And whoa! How dare the Germans call the U.S. “currency manipulators!” Oh the humanity of it, can you believe it? I’m shocked!

And so the majority of the G20 agrees not to manipulate their currencies lower, which leaves the U.S. dollar to tank on its own (with the British Pound), because we all KNOW that in fact this “Fed” and administration are THE biggest manipulators of markets the world has ever known. This is exactly what “QE” is, it manipulates the bond market directly which frees up money to manipulate equities and commodities, all the while intentionally crushing the value of the dollar. Hello $4 gasoline and $12 hamburgers. Every time you eat, you will be paying back the debt with interest, in effect handing over your productive capacity to the oligarchs. It’s a hard chain to follow for most people, but it’s a fact and it’s way past time to wake up to the reality.

And Gary Shilling says that home prices WILL drop another 20% over the next few years sinking the number of homeowners who are underwater from the already horrific 23% to the Noah build an Ark level of 40%!

Got equity?

Existing home sales come out at 10 Eastern, and it may not be too impacted yet by the foreclosure freezes as sales (or the lack thereof) take a while to work through the system. The big data point of the week comes on Friday with Q3 GDP. The consensus is looking for a RISE from the laughable 1.7% to 2.0%! This is the joke of the century, for if the data were truly corrected for the fall of the dollar it would be hugely negative – and if it was corrected for financial engineering it would SHOCK the world at how little we actually produce. Look for this figure to be manipulated higher since it is right in front of the election, and then it will subsequently be revised lower. Consumer Confidence and Sentiment are both released this week, look for these to not reflect the artificial heights of the stock market nor the artificial “growth” numbers.

The HFT machines managed to create two flash crashes just after the close on Friday. One took the Russell 2000 futures lower, the other took the dollar futures flashing down to the 74.6 level:

These flash crashes are an indication of a marketplace that is extremely thin on volume and run solely by computers. It is an artificial market, it is held up entirely on electrons and financial engineering, there is very little fundamental value to support prices at this level. Expose the entirety of the financial FRAUD, and there may very well be an overall NEGATIVE value in the stock market! AHHH, did I really say that? Yes I did. The entire market is built upon a foundation of creative financial engineering and accounting fraud. Take that out and there is very little left to base our stock market, our dollar, our debts upon.

And just look at what the oil and gold charts are showing. Oil is forming a bullish flag worth about $10 a barrel. If it breaks higher we’re looking at $93 per barrel oil:

That’s not a done deal yet, the markets would have to continue to hold together for that, and we are oh so overextended! Just look at the percent of stocks above their 50 day moving average! When this figure gets above 90%, as it is now, there is a very high correlation to market tops:

There is potentially a megaphone top being put in place. It’s not that large of one, and it’s not perfectly formed in all the indices, but it’s potentially in play, so I’m showing it below in red on a 30 minute SPX chart. This pattern may be fairly close to completion:

Some of the momo stocks and commodities are entering what appears to be a parabola. Those create very dangerous and difficult trading opportunities – be careful! Contrast that with what’s occurring to the charts of the financials and you will see that this is not broad and it is not supported – it is therefore FALSE. You can click your heels together and wish yourself over the rainbow all you want, it’s not going to change the fundamental reality of our collective predicament…

Remember this tune? Bill Still used it at the end of his film, The Secret of Oz. I understand that he had permission from Ava’s mother, but in corporations infinite lack of wisdom but infinite power and control, EMI wanted $50,000 from Bill to use it, so he was forced to remove it from the film. This changes all the links to the film, you can now find it here sans the tune above – someone’s dream is coming true: http://www.youtube.com/watch?v=U71-KsDArFM

It’s a Monday... so naturally equity futures have been ramped higher on the back of a dollar that is being crushed. Bonds are soaring higher in a schizoid quantitative fit, the Yen is reaching new completely out of order heights, Oil is reaching for $83 a barrel, and gold is climbing again evidently leaving its mini-correction behind.

And just look at all the manipulation that occurs when you put the G20 together for a weekend! Oh yeah, the IMF “good guys” are going to reorganize to give more power to the emerging markets and they are going to open up its membership to “voting.” LOL, AS IF they are even some type of legitimate organization, THEY ARE NOT, they have as much legal basis as MERS (none), and the U.S.’s participation with the DEBT PUSHING CRIMINALS is not sanctioned by the people of the United States. Giving more power to “emerging markets” is telling us loud and clear that means LESS POWER for the United States! It means the oligarchy who are robbing America blind (same people who own the big banks here, they own the Fed, they own the politicians, they own the exchanges, they own the HFT computers, they own the media, and they own the military industrial complex!!!), are simply packing up their U.S. operations (as we are now debt saturated) and they are moving to take advantage of the next group of as of yet unsaturated saps who have yet to learn better.

And whoa! How dare the Germans call the U.S. “currency manipulators!” Oh the humanity of it, can you believe it? I’m shocked!

And so the majority of the G20 agrees not to manipulate their currencies lower, which leaves the U.S. dollar to tank on its own (with the British Pound), because we all KNOW that in fact this “Fed” and administration are THE biggest manipulators of markets the world has ever known. This is exactly what “QE” is, it manipulates the bond market directly which frees up money to manipulate equities and commodities, all the while intentionally crushing the value of the dollar. Hello $4 gasoline and $12 hamburgers. Every time you eat, you will be paying back the debt with interest, in effect handing over your productive capacity to the oligarchs. It’s a hard chain to follow for most people, but it’s a fact and it’s way past time to wake up to the reality.

And Gary Shilling says that home prices WILL drop another 20% over the next few years sinking the number of homeowners who are underwater from the already horrific 23% to the Noah build an Ark level of 40%!

Got equity?

Existing home sales come out at 10 Eastern, and it may not be too impacted yet by the foreclosure freezes as sales (or the lack thereof) take a while to work through the system. The big data point of the week comes on Friday with Q3 GDP. The consensus is looking for a RISE from the laughable 1.7% to 2.0%! This is the joke of the century, for if the data were truly corrected for the fall of the dollar it would be hugely negative – and if it was corrected for financial engineering it would SHOCK the world at how little we actually produce. Look for this figure to be manipulated higher since it is right in front of the election, and then it will subsequently be revised lower. Consumer Confidence and Sentiment are both released this week, look for these to not reflect the artificial heights of the stock market nor the artificial “growth” numbers.

The HFT machines managed to create two flash crashes just after the close on Friday. One took the Russell 2000 futures lower, the other took the dollar futures flashing down to the 74.6 level:

These flash crashes are an indication of a marketplace that is extremely thin on volume and run solely by computers. It is an artificial market, it is held up entirely on electrons and financial engineering, there is very little fundamental value to support prices at this level. Expose the entirety of the financial FRAUD, and there may very well be an overall NEGATIVE value in the stock market! AHHH, did I really say that? Yes I did. The entire market is built upon a foundation of creative financial engineering and accounting fraud. Take that out and there is very little left to base our stock market, our dollar, our debts upon.

And just look at what the oil and gold charts are showing. Oil is forming a bullish flag worth about $10 a barrel. If it breaks higher we’re looking at $93 per barrel oil:

That’s not a done deal yet, the markets would have to continue to hold together for that, and we are oh so overextended! Just look at the percent of stocks above their 50 day moving average! When this figure gets above 90%, as it is now, there is a very high correlation to market tops:

There is potentially a megaphone top being put in place. It’s not that large of one, and it’s not perfectly formed in all the indices, but it’s potentially in play, so I’m showing it below in red on a 30 minute SPX chart. This pattern may be fairly close to completion:

Some of the momo stocks and commodities are entering what appears to be a parabola. Those create very dangerous and difficult trading opportunities – be careful! Contrast that with what’s occurring to the charts of the financials and you will see that this is not broad and it is not supported – it is therefore FALSE. You can click your heels together and wish yourself over the rainbow all you want, it’s not going to change the fundamental reality of our collective predicament…

Remember this tune? Bill Still used it at the end of his film, The Secret of Oz. I understand that he had permission from Ava’s mother, but in corporations infinite lack of wisdom but infinite power and control, EMI wanted $50,000 from Bill to use it, so he was forced to remove it from the film. This changes all the links to the film, you can now find it here sans the tune above – someone’s dream is coming true: http://www.youtube.com/watch?v=U71-KsDArFM

Open Weekend Thread...

By popular request, this thread is a place to post weekend observations and have discussions with others on wide-ranging topics.

Morning Update/ Market Thread 10/22

Good Morning,

Equity futures are higher this POMO day, with the dollar slightly lower, bonds dropping like a stone in price, oil stubbornly higher and above $80 a barrel still, and gold is down further in its correction.

There is no significant release of economic data today, just a significant release of the people’s dollars to the banking criminals in exchange for their fraudulent “assets.” Next week’s big data release will be massaged attempt #1 in attempting to convince you that a rapidly deflating economy is actually growing – in other words Q3 GDP. Only when measured in dollars – same goes for the stock market.

The long bond’s price action looks very bearish. However, there is a large triangle that may have formed, and if so we are near support on that now. I’m watching this lower trendline to see if it holds or if it breaks:

There was a small move in the McClelland Oscillator yesterday (it’s still negative) which means we can expect a large price move in equities either today or tomorrow.

Yesterday there was yet another flash crash in the markets, only this time it was up which makes it a flash smash. Of course when prices flash to the downside they immediately step in and reverse the trades – not so when prices flash up, here’s a snippet from ZH on what happened:

In other words, what’s happening is that the crooks are manipulating the price of the stock, plain and simple. They belong in jail, but they are obviously above the law. Thus the breakdown of the rule of law is again on public display, yet another blow to confidence in the “market.” Again, it’s not a market, it’s a simulation designed to separate you from your money.

Meanwhile the politicians act as if they are helpless. Still no adults to be seen…

Foreclosuregate is the real deal, make no mistake. It is simply another way of uncovering the true nature of the banks health, a continuation of the cancer that is metastasizing. There are severe moves directly ahead. When the banks are threatened, they will lash out. They will get their way or they will take the markets and the economy down – the direct result of the failure of the people to maintain control over their own money system. There is simply NO WAY to fix and to repair all the damage done to the property ownership trail. Thus there is going to be a push of some type to blanket cover it all up. My best guess would be that the criminals push the government to directly refinance as many mortgages as possible with the government guaranteeing title. This, of course, will simply be another crime against the people, but it will be spun and cloaked in the mask of lower interest rates and the hapless public will gladly go along for the lower monthly payment, debt saturated, bankrupt nation ride. Hell yeah, I want my 2% loan and I want it now!

As I look at the price action yesterday and at the candlesticks of the past two weeks, all I see is a market that is in the same exact position as it was prior to the May flash crash. Every candlestick looks like a top. Every attempt for prices to decline is met with some new scheme – some “Fed” lackey flaps his or her gums, a POMO comes in to provide billions to the criminals, the data comes in massaged, something, anything as long as the market doesn’t do its job of true price discovery. CLINK! Goes the can. Call me your “educated eggdicator.” I simply await the inevitable.

Equity futures are higher this POMO day, with the dollar slightly lower, bonds dropping like a stone in price, oil stubbornly higher and above $80 a barrel still, and gold is down further in its correction.

There is no significant release of economic data today, just a significant release of the people’s dollars to the banking criminals in exchange for their fraudulent “assets.” Next week’s big data release will be massaged attempt #1 in attempting to convince you that a rapidly deflating economy is actually growing – in other words Q3 GDP. Only when measured in dollars – same goes for the stock market.

The long bond’s price action looks very bearish. However, there is a large triangle that may have formed, and if so we are near support on that now. I’m watching this lower trendline to see if it holds or if it breaks:

There was a small move in the McClelland Oscillator yesterday (it’s still negative) which means we can expect a large price move in equities either today or tomorrow.

Yesterday there was yet another flash crash in the markets, only this time it was up which makes it a flash smash. Of course when prices flash to the downside they immediately step in and reverse the trades – not so when prices flash up, here’s a snippet from ZH on what happened:

Today's flash smash comes courtesy of microcap company LiveDeal (Nasdaq: LIVE, market cap around $3 MM) where thanks to a rogue (presumably - there are no news in the name) algorithm the stock shoots up from an opening price of $4.79 all that way to $22.25 in about one minute: a gain of 365%, which is too rich even for KKR's new prop group. And no, this is not a fat finger as the QR screen below shows: the algo was busted enough to lift every single offer in a row - there were virtually no downticks for the span of over 15 seconds. The result: 1,679 shorts end up with an almost 400% loss (one of the benefits of unlimited downside shorting). And as the stock has very little liquidity it is very likely that assorted brokers took matters into their own hands and force covered all those who were underwater and losing substantially. And the cherry on top: not a single trade has been busted. In other words, exchanges are more than happy to unwind trades immediately when an algo loses money, but when an algo creates thousands of forced buy ins and retail investors are left with huge losses, then no luck on the DK. What is scariest is that HFT has now gone microcap: with Apple, Amazon, BofA and Netflix bled dry, it is about time the robotic scalping crew found new pastures.

In other words, what’s happening is that the crooks are manipulating the price of the stock, plain and simple. They belong in jail, but they are obviously above the law. Thus the breakdown of the rule of law is again on public display, yet another blow to confidence in the “market.” Again, it’s not a market, it’s a simulation designed to separate you from your money.

Meanwhile the politicians act as if they are helpless. Still no adults to be seen…