Equity futures went lower, then higher on the Employment situation release. The dollar is lower, bonds are up a little so far, oil is flat, and gold is slightly higher.

As I expected, the headline number was worse than consensus, coming in at -95,000 jobs. There were supposedly 64,000 private jobs created, this is worse than August’s 67,000 and far worse than the consensus of 85,000. The Unemployment Rate remained level at 9.6%.

Here’s the entire report from the BLS:

Employment September

Right off the bat we can see the wave C mentality as the government lost 159,000 jobs. Why? Because the same levels of stimulus are no longer palatable because it is finally being recognized that we have far too much debt.

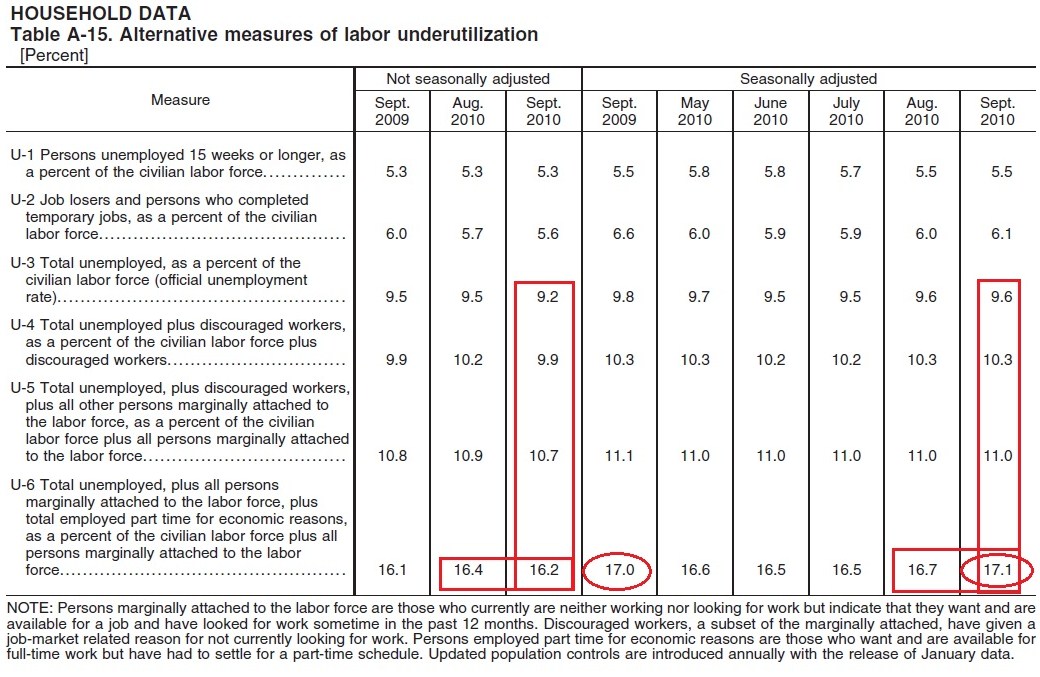

Just look at all the numbers that increased… Sadly, “The number of persons employed part time for economic reasons (sometimes referred to as involuntary part-time workers) rose by 612,000 over the month to 9.5 million. Over the past 2 months, the number of such workers has increased by 943,000. These individuals were working part time because their hours had been cut back or because they were unable to find a full-time job.”

Also, “About 2.5 million persons were marginally attached to the labor force in September, up from 2.2 million a year earlier.” Gee, that’s only an increase of another 300,000 in one month!

And, “Among the marginally attached, there were 1.2 million discouraged workers in September, an increase of 503,000 from a year earlier.”

Those are some dramatic increases, much larger than we’ve seen recently. I do not see a large change to the Employment Population Ratio, it is obvious that the rate was able to stay low due to the large increases in the number sets just above.

Here’s a portion of Econoday’s update:

Highlights

The private sector is doing its best to offset weakness in the government sector. But Census layoffs and state and local government cut backs have been more than offsetting. Payroll employment in September declined 95,000, following a revised 57,000 dip in August and a 66,000 decrease in July. The September fall was significantly more negative than the median forecast for an 8,000 decrease. The July and August revisions were net down a slight 15,000.

The Census Bureau layoffs of temporary workers continued to damp overall jobs. Government payrolls declined 159,000 after decreasing 150,000 in August. A decline in federal government employment was due to the loss of 77,000 temporary Census 2010 jobs. As of September, about 6,000 temporary decennial census workers remained on the federal government payroll, down from a peak of 564,000 in May. Employment in local government decreased by 76,000 in September with job losses in both education and non-education.

But on the positive side, private nonfarm employment continued to rise, advancing 64,000 in September, following a revised increase of 93,000 the prior month. The median market forecast was for an 85,000 boost for private payrolls.

Private service-providing jobs gained 86,000 after an 83,000 increase in August. The rise was led by a 38,000 boost in leisure & hospitality jobs. Other increases were scattered by category. Temp help services advanced another 17,000 after gaining 18,000 in August. This category typically is a leading indicator for permanent job hires or layoffs but companies are still more skittish than usual about adding permanent positions.

Goods-producing jobs fell 22,000 after a 10,000 increase in August. Manufacturing slipped 6,000 while construction jobs dropped 21,000. Mining rose 6,000.

Average hourly earnings were unchanged in September after rising 0.3 percent in August. The September figure fell short of the market estimate for a 0.1 percent gain. The average workweek for all workers was steady at 34.2 hours in September, matching expectations.

On a year-ago basis, overall payroll jobs improved up to 0.3 percent in September from up 0.2 percent the month before.

Turning to the household survey, the unemployment rate was unchanged at 9.6 percent, coming in a little lower than the market forecast was for a 9.7 percent.

Overall, business demand for labor is sluggish. Discounting the loss of temporary Census workers, the recovery continues but at a soft pace.

On the news, Treasury yields and equity futures were little changed. The dollar declined.

Looking at the Alternate Table, we can see that seasonally adjusted U-6, the number most closely resembling how it has been tracked in the past, rose to 17.1% from 16.7%. Note that this is worse than last year’s 17.0%. How many jobs were “created” in the past year?

I have been mentioning that this report would be worse than expected due to the Birth/ Death model. That’s exactly what happened as the adjustment was only 11,000 for September this year which is still more than the zero correction this month last year. Note that next month is a mild correction and then there’s a negative correction coming in November – yes, these do tend to follow this same pattern:

The Birth/ Death model is simply a ridiculous notion and a way for the BLS to manipulate the data. It is not accurate when the economy is contracting or expanding, which would be all the time. That means this model is never accurate! To say that small businesses are adding jobs while small businesses in general are going out of business is simply a lie and an economic distortion.

Below is John Williams Employment chart from ShadowStats.com, you can see that it has now exceeded 22%!

These are depression era readings people, this is no “recession.”

And recently Bernanke so much as admitted that adding QE money will do little to help! Can you say, Wave C mentality?” I thought you could!

Fed’s $2 Trillion May Buy Little Improvement in Jobs

Oct. 7 (Bloomberg) -- For $2 trillion, Federal Reserve Chairman Ben S. Bernanke may buy little improvement in growth, employment or inflation over the next two years.

Firms with large-scale models of the U.S. economy such as IHS Global Insight, Moody’s Analytics Inc. and Macroeconomic Advisers LLC project only a moderate impact from additional Fed asset purchases. The firms estimate that the unemployment rate will remain around 9 percent or higher next year whether the Fed buys $500 billion or $2 trillion of U.S. Treasuries in a second round of unconventional stimulus.

“This is not a game changer for the economic outlook,” said Nigel Gault, chief U.S. economist at IHS Global Insight in Lexington, Massachusetts, whose models show that $500 billion of purchases would boost growth 0.1 percentage point in 2011 and leave the unemployment rate at 9 percent or above for the next two years. “There is clearly a risk that people start to perceive monetary policy as impotent.”

The meager impact shows the conundrum U.S. central bankers face. Interest rates near zero have failed to produce the intended cycle of borrowing and spending among consumers and businesses. Unemployment hovering near a 26-year high, partly a symptom of weak demand, keeps downward pressure on prices, and further declines in inflation would raise borrowing costs in real terms, making credit more expensive.

Uh, huh. They can QE all they want, but if they don’t help those who are saturated with debt, this economy is going exactly nowhere. In fact, it is quite the opposite. If they simply do nothing then the debts will clear and the economy will move forward. It’s their attempts to help it that are destroying it. Each infusion simply lowers the value of our money making it harder and harder for folks to live. The more they do it, the WORSE the economy gets.

Wholesale Trade numbers are released at 10 Eastern this morning.

There are signs from yesterday that the market may finally be rolling. The dollar may have hit at least a temporary bottom, and the Euro a top. I’m basing that simply on the candlesticks that were created and on the Key Reversal that occurred in both oil and gold yesterday. Below is a chart with the dollar on the left and Euro on the right:

The fly in that ointment is the Yen. Yesterday it broke down (down is higher on this chart) below a very power trendline than comprised the bottom of a large descending wedge. I warned yesterday that prices can waterfall out of descending wedges, and today it is continuing to strengthen – that will pressure the dollar and other currencies. This type of move in the Yen is very unwelcome and it has the potential to get disorderly:

The point & figure diagram for the Yen is targeting 151. That target is 25% higher than current levels!

The Japanese yesterday did announce yet another stimulus program although they swear they are going to keep them smaller in the future, LOL. They are hosed, there is no other way to put it, but it was their own actions that put them in their current predicament.

Yesterday the McClelland Oscillator finished barely above zero. Turning negative is a warning sign, one that puts the Hindenburg Omens in play. This is a very dangerous time for equities. Alcoa and Micron both reported earnings yesterday. While Alcoa met their revised expectations, get this… “which declined 21% from the year-earlier period and 55% from the previous quarter. " And Micron (MU), while earning more than last year, flat out missed on both earnings and revenues.

No, QE 666 won’t bring our economy back, our money will be destroyed long before we get there. This employment report is all bad. There is no POMO scheduled for today, the key level is the 1150 mark.